The economic calendar for today is very rich and full of important economic data related to the economies of Australia, Japan, France, Germany, Eurozone, UK and US. The forex market will evaluate the expansion and growth of the manufacturing, services and composite sectors in the Eurozone and in US, and assess the relative attractiveness of the two major global economies. A strong focus later on during the day is on the FOMC minutes, as they can influence significantly the US Dollar upon their release. Overall moderate to high volatility is expected today in the forex market for the Euro, the British Pound and the US Dollar.

These are the main economic events for today in the forex market to focus on:

European Session

- Netherlands Consumer Confidence, France Markit Manufacturing PMI Flash and Markit Services PMI Flash, Germany Markit Services PMI Flash and Markit Manufacturing PMI Flash

Time: 05:30 GMT, 08:00 GMT, 08:30 GMT

Higher than expected or rising figures for the consumer confidence in Netherlands and the various Markit figures for the manufacturing and services sectors will be positive and supportive for the Euro, reflecting economic expansion, increased business conditions and higher growth. The forecasts are for declines for all Markit figures, which are considered a negative fundamental factor and may influence negatively the Euro upon their economic release.

- Eurozone Markit Manufacturing PMI Flash and Markit Services PMI Flash

Time: 09:00 GMT

As before, the forecasts are for a decline both for the Eurozone Markit Manufacturing PMI Flash with a reading of 60.8, lower than the previous reading of 61.1 and the Eurozone Markit Services PMI Flash with a reading of 57.8, lower than the previous reading of 58.0. Although the declines are marginal, they may weigh negatively on the Euro, and any economic surprises, either positive or negative can influence significantly the Euro. It is worth mentioning that Eurozone PMI ended 2017 on a high with a record manufacturing growth, so this small decline may be due to seasonality reasons, and should be monitored in the future months to evaluate if the Eurozone is picking up further momentum which can have a positive impact on economic growth.

- UK Unemployment Rate, Claimant Count Change, Employment Change, Average Earnings Including Bonus

Time: 09:30 GMT

A series of very important fundamental data for the UK economy, as lower readings for unemployment rate and claimant count change indicate a robust labor market and in general lead to higher economic growth, as more people are employed and therefore consumer spending should increase over time leading to higher figures of GDP growth rate. The forecasts are for an unchanged reading of 4.3% for the Unemployment Rate, an unchanged reading of 2.5% for the Average Earnings Including Bonus, and a small increase for the figure of the Claimant Count Change to 8.8K, higher than the previous reading of 8.6K, while the Employment Change is expected to increase at 110K, higher than the previous reading of 102K. Lower figures for the Claimant Count Change are positive for the British Pound as they reflect the number of people seeking actively for a job. Still the higher than expected Employment Change should be considered positive and supportive for the British Pound, indicating a positive momentum in jobs creation.

This statistic shows the forecasted unemployment rate in the United Kingdom (UK) from 2016 to 2021. The rate is expected to experience a net increase over this period, with little fluctuation between 2016 and 2022. The total decrease over this period is expected to be 0.3 percent, with the largest annual decrease occurring between 2015 and 2016, dropping by 0.5 percent. By 2017 and 2018 the unemployment rate is predicted to shrink to 5 percent before increasing incrementally in the following years. Yet despite this slight increase to the rate of UK unemployment the unemployment has been decreasing annually since 2011.

American Session

- US Markit Manufacturing PMI Flash, Markit Composite PMI Flash, Markit Services PMI Flash, Existing Home Sales, FOMC Minutes, US API Crude Oil Stock Change

Time: 14:45 GMT, 15:00 GMT, 19:00 GMT, 21:30 GMT

The forecasts for the US PMI figures are mixed, with a decline for the Manufacturing PMI, and increases for the Composite PMI and Services PMI readings. As in the case of the Eurozone, Germany and France, higher than expected or rising figures will be positive for the local currency, the US Dollar, reflecting economic expansion and higher economic growth.

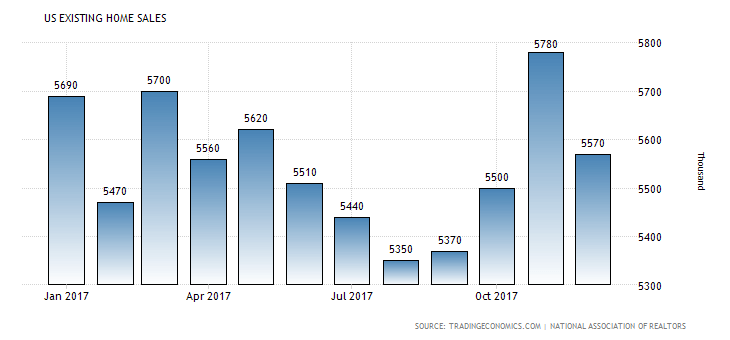

The figure of the Existing Home Sales can also influence significantly the US Dollar as it reflects the strength of the housing market, being a key indicator of the broader economy. The forecast is for an increase of the Existing Home Sales, which should be supportive for the US Dollar. As seen the trend of the Existing Home Sales in the US is volatile, but as of the late summer of 2017, the trend in general is an uptrend, with a decline only during the past month.

The US API Crude Oil Stock Change provides an overview of the US Petroleum demand. In general if the increase in crude inventories is more than expected, then this implies a weaker demand and is considered negative for crude oil prices.

Pacific Session

- Australia Wage Price Index and Construction Work Done

Time: 00:30 GMT

Increased figures for both economic data are considered positive for the Australian Dollar reflecting a strong labor market and increases in wages, which can increase the consumer spending, while a higher construction activity will indicate a robust construction sector, a leading indicator of economic activity. Low or consistent declines in the Construction Work Done may be an early indicator of an imminent contraction in the economy.

Asian Session

- Japan Nikkei Manufacturing PMI Flash, All Industry Activity Index

Time: 00:30 GMT, 04:30 GMT

The forecast for the Japanese Manufacturing PMI Flash reading is for a marginal decline, a reading of 54.5, lower than the previous reading of 54.8, while a higher than expected or rising figure for the All Industry Activity Index, which measures the change in the total production by all sectors of the Japanese economy, will be positive and supportive for the Japanese Yen, reflecting a strong economy with increased economic and business conditions.