The US dollar rally was short-lived but it was the Euro which had a nice rally yesterday based on a combination of economic and political news. But volatility is all about trading opportunities, it is not bad.

Euro

The EUR Markit Services and Composite PMI for many European countries for the month of April 2017 such as Italy, and Germany were better than expected, only France did not meet expectations and this in combination with the Eurozone Markit readings for Services and Composite PMI, which beat expectations were enough good news for the Euro to start on a positive note the whole day.

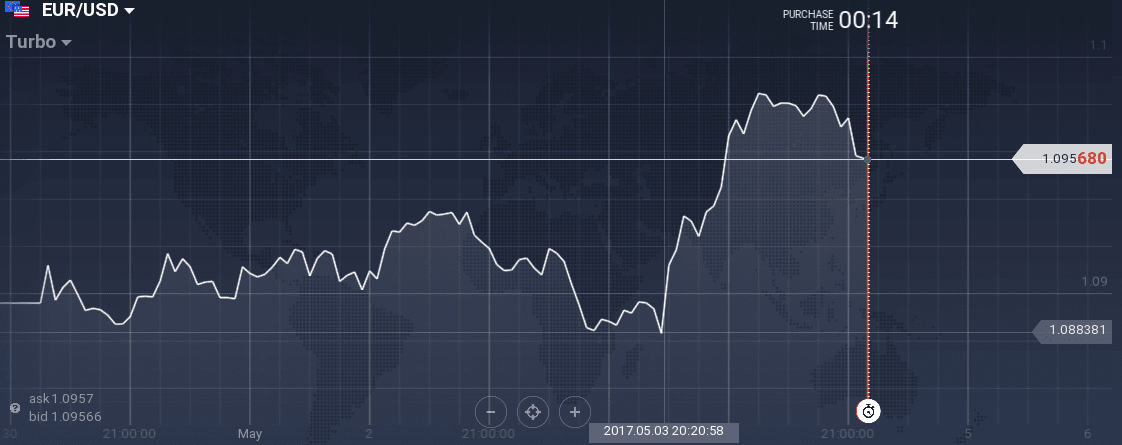

Later on strong Euro-Zone retail sales for the month of March 2017 showing continuing strength in the European economy was a strong factor to push the Euro higher for the rest of the day. The EUR/USD bounced from 1.0873 to 1.0986 yesterday, and there was a positive sentiment due to political reasons as well due to the forthcoming second round of French elections.

The possibility that macron will win is considered the best case scenario for the Euro and this was reflected strongly yesterday. The main question and risk for the Euro now is if the market has discounted already the win of Macron, what factors can continue to its recent strength?

British Pound

The British Pound had also better than expected Markit Services and composite PMI readings for the month of April 2017, and it is no surprise that it moved higher following the Euro and the GBP/USD ended the day up to 1.2930 from the low price of 1.2829.

Continued strength in UK economy is a positive factor for the Pound, but again with forthcoming UK elections the market may already has priced the win of Theresa May so again there is a question which catalyst can move the Pound higher.

US Dollar

A day with mixed economic news for the US dollar as US Trade Balance deficit for March 2017 was lower than expected, and weekly Initial Jobless Claims and Continuing Claims were less than expected, and this is positive, bullish for the dollar.

![]()

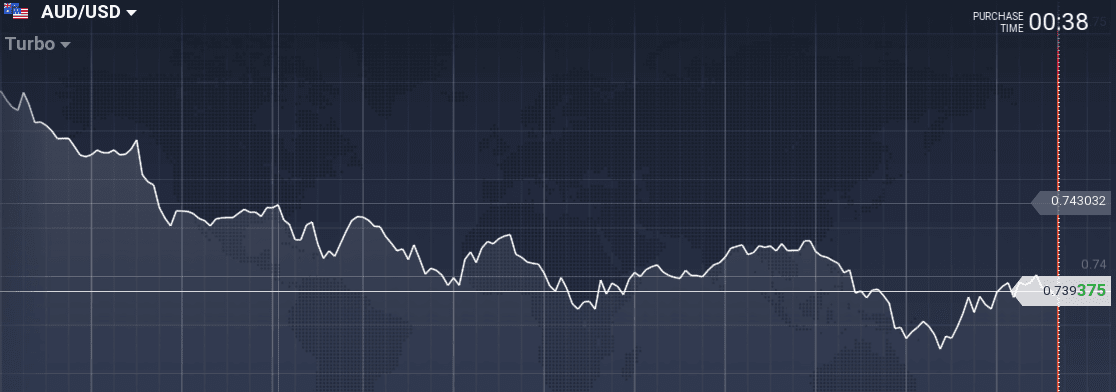

The labor market seems strong enough. However Factory Orders for the month of March 2107 were less than expected, while Durable Goods Orders were better than expected. The US dollar managed to appreciate versus the Australian dollar as the AUD/USD pair moved yesterday lower from 0.7430 to 0.0.7380.

But the US dollar did not mange to continue strengthening against the Japanese Yen as the USD/JPY moved lower from 113.038 to 112.30, something that can be attributed to profit-taking as the USD/JPY has moved up all this current week.

Swiss Franc

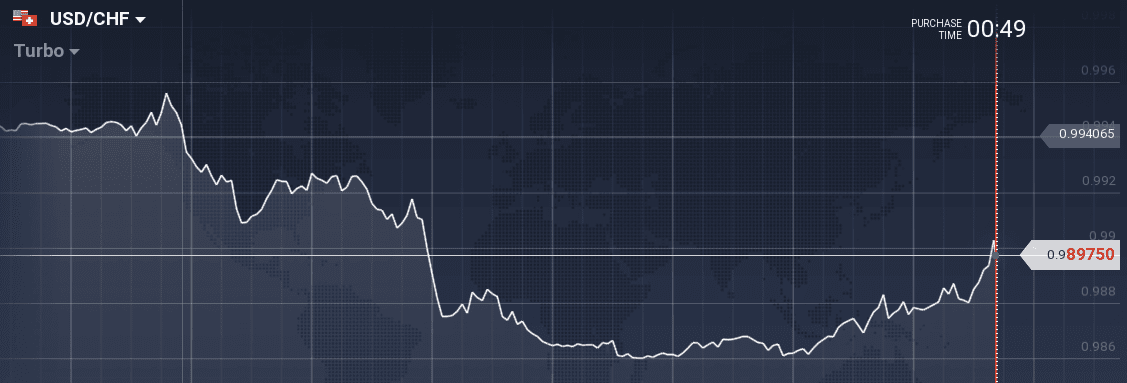

A very interesting day for the Swiss Franc as the USD/CHF pair moved down from 0.9949 to 0.9856 while gold price fell significantly, over 1.50%.

The positive correlation between gold price and Swiss Franc does not hold 100% all the time.

Canadian Dollar

As oil prices fell again, over 3% yesterday the Canadian dollar seems weak and the USD/CAD moved up to 1.3775 from 1.3698. As long as oil prices continue falling, the Canadian dollar probably will continue weakening against major currencies. Today however there is the important Unemployment Rate for Canadian economy and if there is a positive surprise, we may have a reversal to the Canadian dollar decline.

Today is a day that is dominated by very important US dollar fundamental news as there is at 12:30 GMT the Non-farm Payrolls, the monthly Unemployment Rate and the Average Hourly Earnings. All this data is extremely important as there will be clues whether a positive surprise to the health of labor market can make the FED decide to implement another interest rate hike next month. It is an unpredicted day with often significant volatility so it is suggested due to the high risk for traders to avoid trading US dollar pairs around 12:30 GMT. Often the US Non-farm payrolls set a tone and define trends for the whole following weeks or month.

{kind=link}

{kind=link}

{kind=link}

{kind=link}