Micron (MU) sits at the center of the AI memory boom — and after a near‑200% run, the real debate is how much of that boom is already in the price.

Micron Technology (MU) is one of the few global makers of DRAM, NAND, and high-bandwidth memory that feed today’s AI data centers, tying its fortunes directly to cloud and GPU build-outs. After a rapid run-up driven by sold-out HBM capacity and record earnings, investors are now weighing how long AI-driven demand can stay this strong before the next memory downcycle hits.

Summary

| Key Fact | Detail |

|---|---|

| Company | Micron Technology (MU) |

| Sector / industry | Semiconductors / memory and storage |

| Market cap | $1.1T |

| YTD return | +196.8% |

| Key catalyst | AI-driven demand for HBM and advanced DRAM |

| Primary risk | Potential memory downcycle and oversupply from rivals |

Data source: Yahoo Finance, as of June 2026.

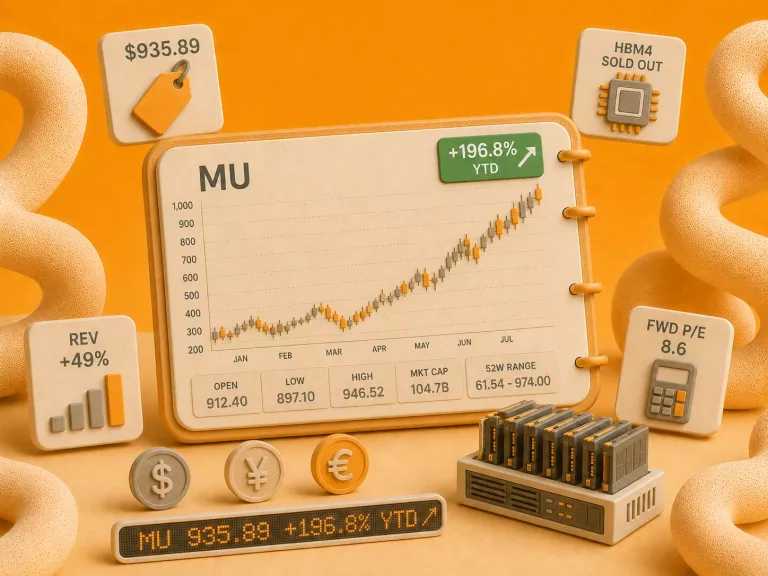

Micron Technology (MU) at a Glance: Key Stats and Fundamentals

| Metric | Value |

|---|---|

| Current Price | $935.89 |

| Market Cap | $1.1T |

| P/E Ratio | 44.3 |

| Forward P/E | 8.6 |

| YTD Performance | +196.8% |

| Dividend Yield | 0.1% |

| 52-Week High | $1,089.29 |

| 52-Week Low | $103.38 |

| EPS | $21.15 |

What Does Micron Technology Do in the AI and Memory Market?

Micron Technology is a leading memory and storage maker that sells chips used to store data in everything from AI data centers to smartphones and cars. It is one of only three companies that can mass‑produce leading‑edge memory — the others being Samsung and SK Hynix — and at about $37.4 billion in annual revenue it has the volume to supply every major AI platform.

Micron’s business model is straightforward: it designs and manufactures memory chips and storage products, then sells them to device makers, cloud providers, and equipment manufacturers. These customers use Micron’s parts in servers, AI accelerators, PCs, smartphones, networking gear, and cars. The company earns most of its money from selling DRAM and NAND in large volumes, so pricing and demand for these chips have a big impact on its results.

In the AI era, Micron has become a key supplier of high-bandwidth memory used in advanced graphics and AI platforms. Its latest HBM4 products are designed to work with leading AI systems such as NVIDIA’s Vera Rubin platform, and Micron’s HBM4 capacity is reportedly sold out under contracts through 2026. This shift moves Micron away from being seen only as a “commodity memory” producer and closer to a strategic infrastructure player for AI data centers.

Within the global memory industry, Micron competes mainly with Samsung and SK Hynix. The market is concentrated, and adding new factories is expensive and slow, which can limit supply and support pricing when demand is strong. With revenue growing nearly 49% year over year and a pipeline of new advanced memory technologies, Micron is positioned as one of the key companies providing the memory backbone for AI and high-performance computing over the next several years.

What Key Forces Drive Micron Technology (MU) Stock Analysis in 2026?

Micron Technology (MU) stock analysis in 2026 centers on how AI-driven memory demand, tight supply, and rapid earnings growth intersect with high volatility and heavy competition. With a near-$1.1 trillion market cap, revenue of $37.4 billion, and year-over-year sales growth of about 49%, Micron is now treated less like a traditional memory maker and more like a core AI infrastructure name. The share price has surged about 197% year to date to near $935.89, and the unusual part is the valuation: 44 times trailing earnings but under 9 times forward earnings — a sign the market expects this year’s profit to be only a fraction of next year’s.

Several distinct forces tend to move the stock:

- AI data center and HBM demand: Q2 FY2026 revenue grew 196% year over year, with gross margins in the mid-70% range, mainly from AI data center demand and tight supply across DRAM, NAND, and HBM. Advanced HBM4 capacity is reportedly fully sold out through 2026 under binding contracts, which supports pricing and earnings expectations.

- Supply tightness and pricing: Management expects DRAM and NAND supply to stay constrained through 2026. DRAM prices rose about 90% in Q1 2026, and Micron generated $1.7 billion in free cash flow over the last year. These conditions often boost margins but can reverse if new capacity comes online or demand cools.

- Macro and rate sensitivity: The stock has shown sharp moves on Federal Reserve signals and geopolitical headlines. A roughly 22% pullback followed Fed hawkishness and profit-taking after a steep run, highlighting how sensitive a high-beta, high-expectation stock can be to broad market risk sentiment.

- Technology and competitive shifts: Micron’s push into HBM4 and future HBM4E for NVIDIA’s Vera Rubin platform and “Agentic AI” workloads supports its positioning, but it still faces intense rivalry from Samsung and SK Hynix. Any sign that competitors gain an edge in bandwidth, power efficiency, or yield, or that memory compression tools like TurboQuant reduce bit demand, can weigh on valuation.

Short term, scheduled catalysts like the June 24, 2026 Q3 earnings report and any updated revenue outlook toward the mid-$30 billion range may drive large price swings. Longer term, investors often watch whether Micron can turn today’s AI boom, tight supply, and premium valuation into sustained earnings power rather than another memory downcycle.

What Gives Micron (MU) Its Competitive Edge in AI Memory?

Micron’s edge in AI memory rests on rapid growth, leading-edge chip technology, and tight supply that supports stronger pricing. Memory is a three‑player game — Micron, Samsung, and SK Hynix — and that concentration is exactly why this cycle behaves differently: when all three are capacity‑constrained at once, none of them has to start a price war to win share. Revenue grew about 48.9% year over year, showing how quickly demand for its memory and storage is ramping with AI data centers and high-performance computing.

Profitability and cash generation also support this competitive position. Micron earns $21.15 in earnings per share, and free cash flow of $1.7B gives the company room to keep funding new fabs and advanced R&D without relying only on debt or new shares. The clearest signal is in the multiples: the stock trades at 44 times the last year’s earnings but only about 9 times next year’s. That collapse in the forward P/E is the market betting that profit explodes as higher‑value AI products like HBM4 take over the mix — far faster than revenue alone would imply.

On the technology side, Micron has moved into the top tier of AI infrastructure suppliers. Its HBM4 products, built on advanced 1-gamma DRAM nodes, are designed for NVIDIA’s Vera Rubin platform and focus on higher bandwidth and lower power use. Management notes that advanced HBM4 capacity is already fully booked under binding contracts through 2026, and DRAM and NAND supply is expected to stay tight, which may give Micron better pricing power than in past memory cycles.

A long-term investment plan underpins this edge. Capital spending is set above $25B in FY2026, with more than $100B committed to future fabs that are not expected to add meaningful capacity until around fiscal 2028. Combined with a modest dividend yield of 0.1% and a YTD return of about 196.8%, these numbers suggest Micron is using today’s AI-driven upswing to build a larger, more durable position in high-value memory for years ahead.

Micron Technology (MU) Stock Analysis: What Are the Biggest Risks for Investors in 2026?

Even with AI demand running hot, several risks could change Micron’s story quickly if that strength cools. The share price has surged, with a year-to-date gain of about 196.8% and a market value around $1.1 trillion, so expectations are very high. At a trailing P/E near 44.3, any sign that earnings are peaking or AI demand is normalizing could lead to a sharp pullback, even though the forward P/E of 8.6 looks lower based on optimistic forecasts.

Cyclicality in memory remains a core risk. Micron’s revenue jumped to $37.4 billion with year-over-year growth near 48.9%, helped by tight supply and strong pricing in DRAM, NAND, and HBM. If AI spending, cloud-server builds, or device demand slow, memory prices could fall, squeezing margins and leaving Micron with expensive factories running below capacity. Aggressive capacity builds by Samsung and SK Hynix, especially in advanced DRAM and HBM, could also swing the market back into oversupply in coming years.

Technology and architectural changes add another layer of uncertainty. If AI models, software tools, or new chip designs cut the amount of memory needed per system, growth in HBM and DRAM demand could come in below current hopes. Micron is committing over $100 billion to new fabs and large annual capital spending, so a demand shortfall would weigh on returns and limit flexibility to handle a downturn.

Regulatory and geopolitical exposure is an ongoing concern. Micron depends on global demand, including sales into China, at a time when US export rules on advanced chips and memory are tightening. New limits on what Micron can ship to certain regions, or broader trade tensions, could reduce its addressable market or force product changes. Combined with the stock’s recent run from a 52-week low near $103.38 to above $900, these factors may increase volatility around earnings reports and macro headlines.

What Key Events Should Investors Watch for in Micron Stock in Q2 2026?

The main things investors are watching for in Micron stock in Q2 2026 are the upcoming Q3 earnings report, any signs of a shift in AI-driven memory demand, and changes in supply or pricing for DRAM, NAND, and HBM. With Micron shares up about 196.8% year to date and trading not far below a 52-week high of $1,089.29, expectations are elevated and the stock may react sharply to new information.

The June 24, 2026 Q3 earnings release is the first big checkpoint. Markets will focus on whether revenue lands near the guided mid-$30B range, if gross margins stay around the low-80% area, and whether management raises or trims the outlook for the rest of fiscal 2026. Any update on HBM4 and HBM4E ramp timing, capacity being sold out (or not), and long-term AI demand assumptions could quickly change sentiment.

Beyond earnings, traders often watch for:

- Memory pricing and supply signals: Updates from Micron or peers on DRAM, NAND, and HBM pricing trends, or signs that supply is no longer tight, could hint at an earlier end to the current upcycle.

- AI capex and hyperscaler spending: Comments from large cloud providers on GPU purchases and AI build-outs directly affect demand for Micron’s advanced memory.

- Geopolitics and regulation: Any new export rules on advanced memory, or restrictions on sales into China, may weigh on Micron’s long-term growth story and could pressure the stock in the near term.

- Upcoming earnings and economic events: Key dates like Micron’s June 24, 2026 Q3 report — and macro releases that move chip demand — are worth tracking on the economic calendar on Trading Dashboard.

How Could Different 2026 Scenarios Impact Micron (MU) Stock?

Micron’s 2026 really comes down to two variables — how much AI memory the market needs, and what it is willing to pay for it. The table below runs bear, base, and bull versions of those two levers and ties them to revenue, margins, and how the stock might react.

| 2026 Scenario | AI Server Demand | DRAM/NAND Pricing Trend | Micron Revenue Direction | Operating Margin Outlook | Possible Stock Reaction | Key Investor Focus |

|---|---|---|---|---|---|---|

| Bear Case | Slower than expected AI build-out | Prices weaken or stay flat | Stagnates or dips vs. 2025 | Margins narrow as costly fabs run below capacity | Could face pressure or trade sideways | Balance sheet strength and cost cuts |

| Base Case | Steady AI infrastructure growth | Gradual price improvement | Grows modestly from 2025 | Margins improve with better factory use | Tracks earnings trend with normal swings | Execution on product roadmap and discipline on spending |

| Bull Case | Faster AI adoption and cloud capex | Prices rise on tight supply | Grows meaningfully above 2025 | Margins widen as scarce HBM and DRAM pricing flows straight to the bottom line | May benefit from stronger re-rating | Capacity planning, supply discipline, and winning AI design wins |

None of these are predictions — they are a way to pressure‑test how much Micron’s 2026 result depends on its two swing factors: AI demand and where memory prices go.

Key Takeaways

- Micron is now an AI‑driven memory leader with $37.4B revenue, 48.9% year-over-year growth, and a $1.1T market cap.

- Micron’s HBM4 and advanced DRAM nodes position it as a key supplier to AI data centers, with high-bandwidth capacity reportedly sold out through 2026.

- Valuation looks stretched on recent performance, with a 196.8% YTD return and trailing P/E of 44.3, even though the forward P/E is much lower at 8.6.

- Heavy capital spending above US$25B in FY2026 and over US$100B in fab commitments may pressure returns if AI memory demand softens.

- Industry risks include a possible memory downcycle, aggressive capacity expansion from Samsung and SK Hynix, and potential oversupply after 2027.

- Regulatory and geopolitical uncertainty around exports to China, plus any slowdown in AI infrastructure spending, could quickly pressure Micron’s margins and share price.

This article is for informational purposes only and does not constitute investment advice. Always do your own research before making trading decisions.