New equity sell-off, changing geopolitical risk in Syria and North Korea, new episodes of tariffs drama and White House drama. All happened in a week that started with a G-20 meeting, a forum where cooperative initiatives are supposed to be taken and coordination is supposed to be achieved.

I do not expect so many events next week, as it is the Holy Week of Catholic Christians.

My last week’s views were not as accurate as older ones.

- Adding to the short EUR/JPY position at 131,20 level paid off

- USD/CAD bounced lower than the expected 1.3150 and did not increased back up from the 1.2976-1.2944 level, so the position is in the red.

- AUD/USD was consolidating and managed to close the week at lower levels, as I was pointing to

- EUR/USD did not move south as I was expecting. Yet the downtrend line has not been crossed

- GBP strengthening scenario is indeed happening as forecasted. Yet no remarked level was triggered so that I could take advantage of it.

Major last week’s events:

- announcement of extension of Brexit deadline

- bombing of Afrin (Syrian city) by Turkey’s forces

- diplomatic talks in Finland, between USA and North Korea officials. At the same time, the scheduled military exercise of South Korea and USA is not postponed, and John Bolton (considered to be a hawk regarding North Korea) replaced current National security advisor

- Powell’s first FOMC meeting as FED’s Governor, initially sent USD lower, yet I strongly believe his communication was hawkish and point to a stronger USD

- New episodes of tariffs drama. EU, Canada, Mexico, Argentina, Australia, Brazil, South Korea were excepting from steel and aluminum tariffs, yet Japan was not except. On Thursday, China’s embassy in USA said, “China is not afraid of and will not recoil from trade war”, China could impose tariffs on 3B$ worth of US trade and could hit US Soybean producers, and USA could impose new tariffs on 50B$ worth of Chinese trade.

I keep betting on the high tension, high volatility, increasing inflation, increasing bond yields, decreasing equities scenario that favors haven currencies.

Major next week events:

- it is the Holy Week for Catholic Christians and no market moving announcement is expected

- Very low trading activity expected on Friday. Usually reversals are unlikely during holiday’s

JPY

My EUR/JPY short bias and most of my last week’s remarks remain valid. The advised 131.20 proved to be a nice entry level and I keep targeting the 127.60-127.10 zone.

Last week’s Trade Balance release (-0.20T JPY) was not part of my scenario. Yet the new equity sell-off and episodes of tariff drama favored JPY and will continue to do so. I regard any retest of the 200-Day Moving Average as an opportunity to go short.

Snapshot:

- 0% GDP growth, all time low unemployment at 2.4%

- Inflation (excluding food-National core CPI) is picking up at 1.0% (vs 2.0% target)

- 05% 10y Bond yields vs BOJ’s target of 0.00% level (next auction on 4th April)

Strengths of JPY:

- decisiveness communicated by the Central Bank. Next meeting is scheduled within the end of April

- Trump’s tariff drama or any other turbulence favors JPY as it maintains it’s safe haven

Weaknesses of JPY:

- North Korea talks and tariffs, would have days with new provocative announcements and days of counter announcements that would diminish the importance and aggressive style of the former ones. I assume that we will witness a more peaceful week ahead, in all fronts.

Watch:

- Tuesday’s (05.00GMT) BOJ core CPI (another inflation reading)

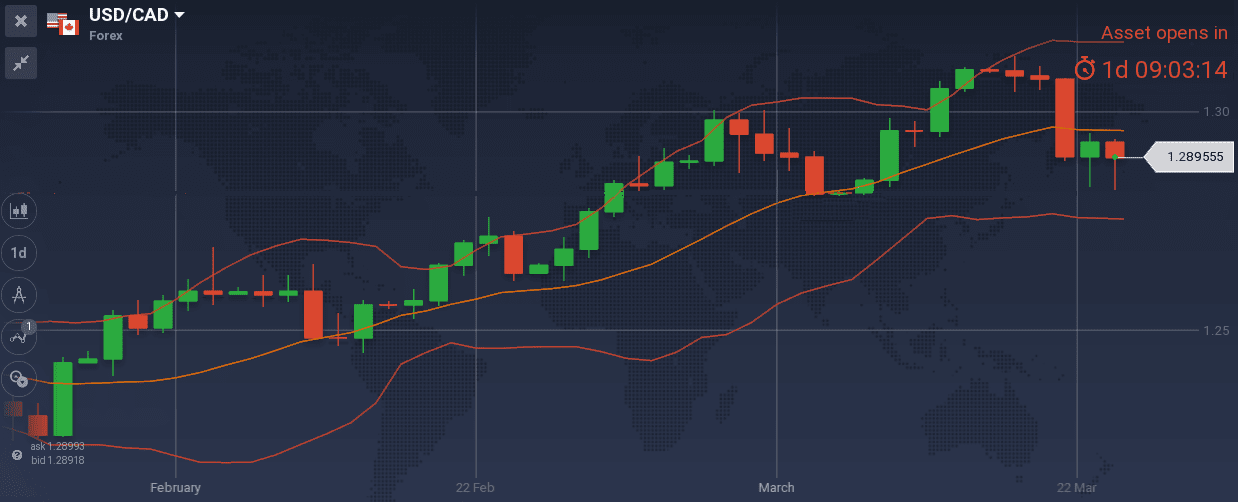

CAD

I am keeping long positions on USD/CAD at higher level than current week’s close. Even if I am wrong with my reasoning that BOC (the Central Bank) will keep rates unchanged on the 18th of April meeting, I strongly believe that there are enough reasons for the pair to retest the 131.50-131.66

Snapshot:

- Inflation at 2.2% (vs 1.0%~3.0% target range). Increased as expected.

- GDP at 2.9% annual, 0.4% qoq, 10Y Government bonds at 2.2%

- Unemployment at 5.8% and expected to increase slightly until the end of the year

- Crude oil prices have strengthened alleviating pressure from CAD.

Strengths of USD/CAD, weakness of CAD:

- Central Bank, needs to price in the outcome of NAFTA talks. I am waiting the release of Business Outlook Survey, expected on 9th of April. Until then, CAD is under pressure.

- I continue correlating any increase of inflation with further weakening of CAD, something that indeed happened last Friday and could continue happening during the week.

- I believe that no rate hike is considered for the next meeting on 18 of April.

Weaknesses of USD/CAD, strengths of CAD:

- Crude oil prices have strengthened, coupled with the unexpected last week’s decrease of US crude oil inventories

Watch:

- Wednesday’s 14:30 GMT US Crude oil inventories. I still believe that any number above 2.5Mbarrels is weakening CAD. Last week the number was unexpectedly negative (-2.6MBarrels) and moved CAD higher (USDCAD lower).

- Thursday’s 12:30GMT monthly GDP announcement

AUD

Increasing unemployment at 5.6% gives another good reason for RBA to not consider tightening any time soon. I have straightforwardly expressed my view that AUD/USD pair is in a well-defined downturn and both the actual move of the pair and the macro releases of last week, strengthen this scenario.

Yet, I do not believe that the downtrend will continue during next week. Most possible scenario is for the pair to consolidate between 0.76 and 0.78 levels

Snapshot:

- Central bank ‘s interest rate is at 1.50% with no hike yet in this cycle.

- Inflation at 1.9% (vs 2.0~3.0% target), Unemployment at 5.6% and expected to decline

- GDP latest reading at 2.4% growth (2.8% was 2017 reading)

Strengths:

- Nothing to note

Weaknesses:

- Latest declined GDP reading

- Declining terms of trade

- Latest increased unemployment reading at 5.6%

- New equity sell-off

Watch:

- No market moving event for the week

- Next Monetary Meeting on 3rd of April, two weeks from now.

- Remember that next release of Australian wages expected on the 16th of May. I believe that this is the only reading that could trigger an updated Central Bank’s view. Note that markets are expecting the first-rate hike no earlier than the first half of 2019.

USD

I keep my 2018 long bias on USD. What I get from FED’s communication is aggressive rate hiking during the year, which I believe is not priced at current USD levels. I am not yet calling for 4 rate hikes within 2018. I do believe that equity sell-offs (like the one we are witnessing now or had witnessed on February) will keep on happening and would put the brakes on FED’s tightening. What I am implying is that an independent/sober/reasonable/ confident interpretation of Wednesday’s FED’s press conference should categorize it as a hawkish communication*. The only question I noticed that the Governor was not persuasive enough was the question regarding the consequences of a possible trade war.

Markets reaction was opposite to my interpretation. It took 14 hours and Thursday’s European Opening (at 08:00GMT) for the markets to start pushing USD higher, which was unreasonably weakening up until that point. To my defense, the new Governor’s (Jerome Powell) quick rhythm of speaking, and more human nature of voice (compared with Draghi’s or Yellen’s extremely cautious/almost nonhuman usage of words) will create some misunderstanding/confusion/opportunity.

USD strengthening was interrupted by Thursday’s new episode of tariffs drama. “China is not afraid of and will not recoil from trade war” was communicated by the embassy of China in USA, China could impose tariffs on 3B$ worth of US trade mainly hitting US Soybean producers, and USA could impose new tariffs on 50B$ worth of Chinese trade.

*for the not experience reader: tightening=raising rates=hawkish actions against rising inflation vs loosening=decreasing rates, or waiting=dovish actions against rising inflation

Snapshot:

- US economy is growing at 2.5% (FED expects 2.7% GDP growth in 2018), unemployment is at 4.1% (FED expects to fall at 3.8% in 2018), inflation measured by PCE is at 1.7% (FED expects 1.9% reading in 2018)

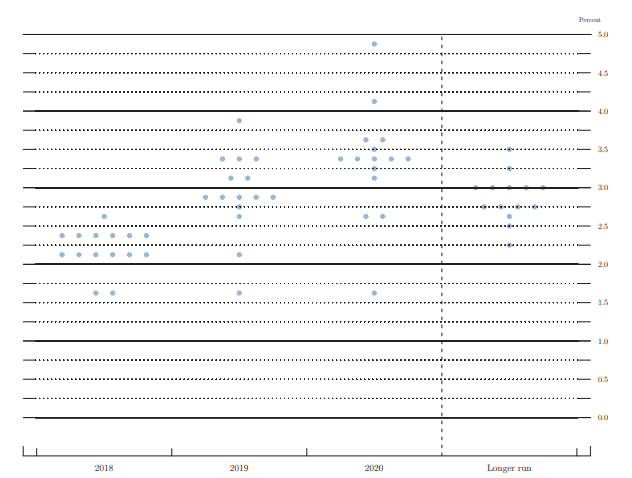

- We are counting 6 hikes of 25bps since Dec ’15, resulting to a current FED rate of 1.75%. FED’s dots are currently pointing to another 6 hikes (peak of 3.25% in this cycle) and FED’s view of long run rate remains at 2.75%~3.00%

Strengths of USD:

- strong macroeconomic announcements and yields Government bonds (now at 2.82%)

Weaknesses of USD:

- Tariffs drama is proving to be the market mover of 2018. Note that, USA has 2.1T$ annual exports, 2.6T$ annual imports. Out of these 130B$ exports go to China (6% of total) and 505B$ imports come from China (20% of total) . Trump is supposed to want to decrease this 300B$ deficit by 100B$

Watch:

- Tuesday’s 14.00GMT consumer confidence reading. I want to see a higher number than the last reading of 130.8 for the reinforcement of my scenario.

- Thursday’s 12.30GMT PCE price index. My scenario wants a higher reading than the last one (i.e. higher than 0.3%mom). Yet a 0.2% number, does not puzzle me, as it is within market’s expectations, and as such it is priced.

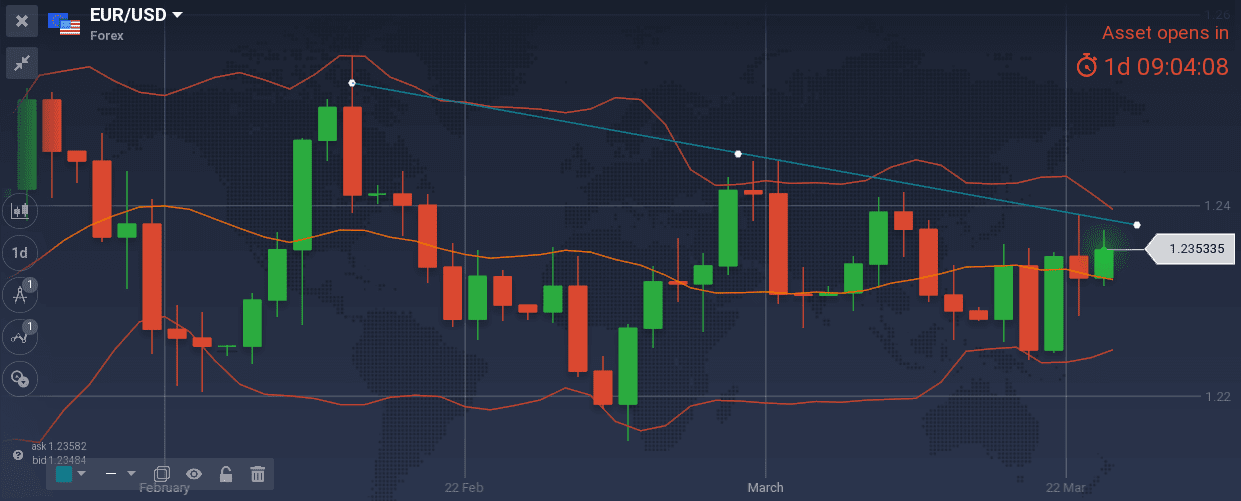

EUR

I am keeping my short bias on EUR/USD. Except for the increased Current Account at 37.6B EUR, all readings are within my scenario. Tuesday’s published economic statement (ZEW at 13.4) has plunged, Wednesday’s German’s 10Y bond auction resulted in lower yields (0.60%), FED’s rate increased by 25bps and all Thursday’s PMI readings were deteriorating. Positioning on the divergence of EUR vs USD makes sense, especially during periods of equity sell-offs

Last week’s mentioned and drawn trend line has not been crossed despite the new episodes of tariffs drama. I believe that the trend line will prove to be valid and that current levels are nice to build a short position.

Snapshot:

- European’s Economy is doing well. Actual GDP growth at 2.4% but the rosy picture seems to have already been priced at the 1.25 peak

Strengths of EUR/USD:

- tariff drama strengthens the pair. With the announcement of steel and aluminum tariffs the pair went up. When tariffs proved to include many exceptions, pair went south. Last week’s new announced tariffs coupled with China’s verbal reaction are pushing the pair back north.

Weaknesses:

- the divergence of EU’s and USA’s economy is becoming more evident as the European government bond’s yields are decreasing and at the same time FED is signaling and delivering further rate hikes in 2018.

- double top formation at the 1.2500 level, and defined formation of downtrend that is still valid

Watch:

- Wednesday’s 10Y Italian Government bond auction. Last reading, just before the elections, was 2.06%.

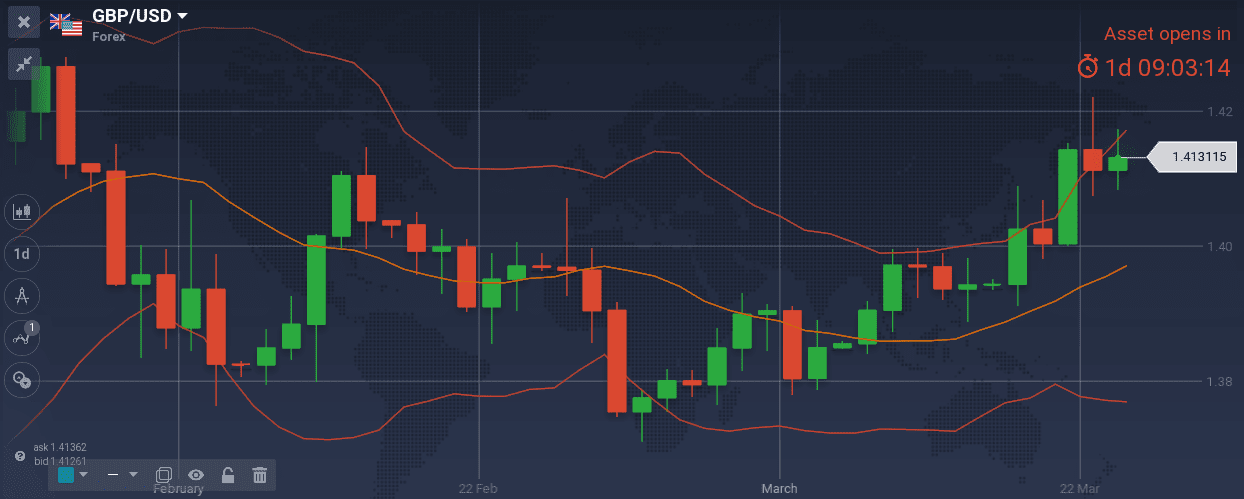

GBP

BOE’s degrees of freedom seem to increase. On the one hand we had the announcement of the extension of the Brexit deadline -it was set on Dec 2020, 21 months later than the initial March 2019 deadline-, the inflation CPI index is finally decreasing (2.70% latest reading). On the other hand, unemployment is at record low (4.3%) and average earnings are picking up 2,8%. The picture is getting rosier.

I believe that being long GBP could pay off:

- I could enter long GBP/USD at 1.3965-1.3930 range

- I could enter long GBP/CAD at the same un-triggered levels I noted last week: 1.8058, 1.8048, 1.8005 or even 1.7950 levels

- I could enter long GBP/AUD at 1.8090, 1.8000 and 1.7955

- I could enter short EUR/GBP at 0.8836 and 0.8805

Snapshot:

- 5% GDP growth, 4.4% unemployment and 2.70% inflation (only major economy with higher inflation than the targeted 2%, but finally now it is decreasing)

- Second rate hike on the 10th of May is turning even more probable.

Strengths:

- Macro announcements showing that the economy is strong

Weaknesses:

- Nothing to note

Watch:

- Thursday’s 08:30GMT Current Account reading