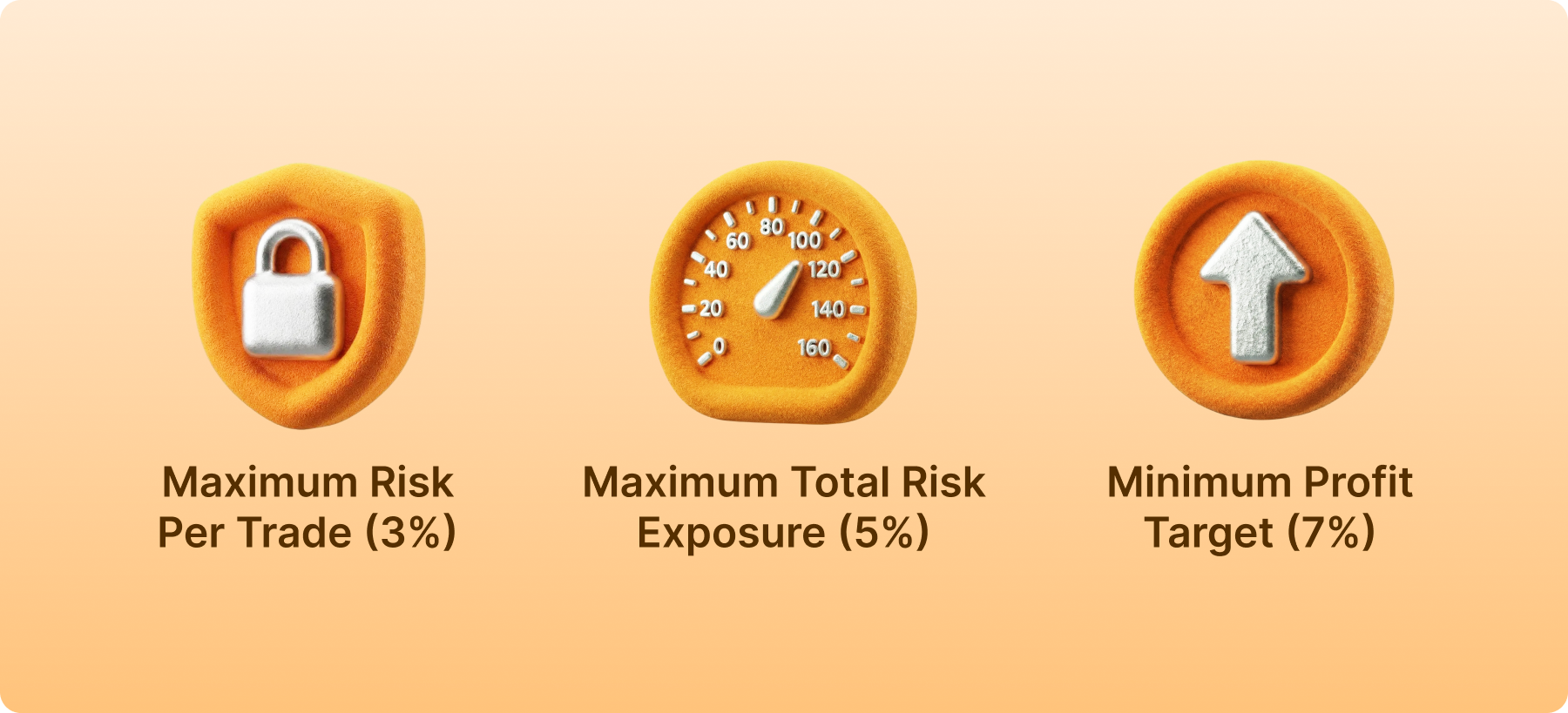

The 3-5-7 Rule is a risk-management framework designed to solve the three most critical problems in trading: position sizing, portfolio exposure and profit expectancy. It is used to ensure that no single loss (or series of correlated losses) can destroy a trading account, while simultaneously mandating that winning trades are large enough to compound capital.

It answers three core questions every trader must solve:

- How much can I lose on one trade? → 3%

- How much risk can I carry across all trades? → 5%

- How large should my winners be? → 7% or more

Rather than reacting emotionally to market movement, this rule forces traders to define risk before entering a trade, not after something goes wrong.

The “3” – Maximum Risk Per Trade (3%)

The first pillar of the rule dictates your Stop-Loss threshold. This 3% limit refers to the dollar amount lost if your stop-loss is triggered, not the total size of your position.

The Survival Math

Most traders fail not because their strategy is bad, but because their “Risk of Ruin” is too high. If you risk 10% per trade, a string of 10 losses wipes you out completely. If you risk 3%, a string of 10 losses (an extreme statistical outlier) leaves you with roughly 73% of your capital—enough to recover.

Calculating Position Size Based on 3%

To implement the “3,” you must work backward from your risk, not forward from your buying power.

The Formula:

Position Size = (Account Equity * 0.03)/(Entry Price – Stop Loss Price)

Real-World Application:

- Account Balance: $20,000

- Max Risk (3%): $600

- Asset Price: $150

- Technical Stop-Loss: $144 (A $6 move)

- Position Size: $600 / $6 = 100 shares ($15,000 total position value)

By using this math, you ensure that if the market moves against you, the damage is capped at exactly $600, regardless of how much the asset price fluctuates.

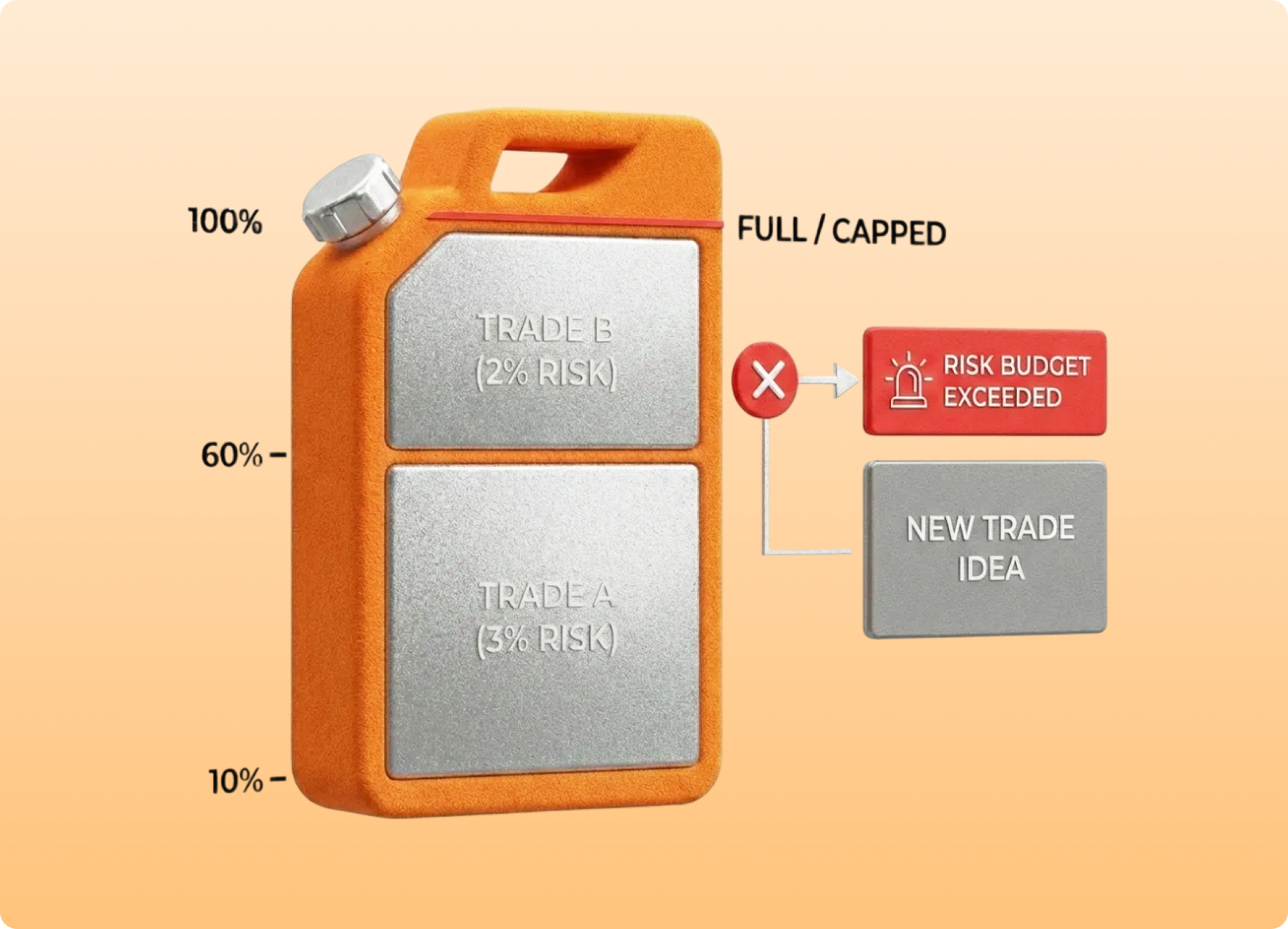

The “5” – Maximum Total Risk Exposure (5%)

The “5” represents your Portfolio Heat. While the 3% rule protects you from a single trade failing, the 5% rule protects you from market-wide correlation.

The Problem with Over-Exposure

In high-volatility environments (Crypto, Tech stocks, Forex), assets often move in lockstep. If you have three separate trades in AI stocks, each risking 3%, your “hidden” risk is actually 9%. If a sector-wide news event occurs, all three stops will hit simultaneously, causing a nearly 10% account drawdown in minutes.

Managing the 5% Ceiling

The 5% rule acts as a circuit breaker for your ego.

- The 2-Trade Maximum: If you have one trade running at full 3% risk, you can only open one more trade with a maximum risk of 2%.

- Earning Your Risk: To open a third trade, you must first move the stop-loss on your initial trades to Break-Even. Once a stop is at break-even, that trade’s risk is 0%, “freeing up” your 5% budget to be used elsewhere.

- The “No-Fly” Zone: If your total open risk is 5%, you are prohibited from taking new entries, no matter how “perfect” the setup looks. This forces you to prioritize quality over quantity.

The “7” – Minimum Profit Target (7%)

The final component moves from defense to offense. The “7” is a benchmark for Positive Expectancy. If you risk 3% of your account to make 7%, you are operating with a Reward-to-Risk (R:R) ratio of 2.33:1.

Why the 7% Threshold is Non-Negotiable

If you risk 3% to make 3% (a 1:1 ratio), you must be right more than 55% of the time just to cover commissions and slippage. Most professional traders have win rates between 35% and 50%.

By mandating a 7% target, the math shifts in your favor:

- With a 40% Win Rate: After 10 trades, you have 4 wins ($28% gain) and 6 losses ($18% loss). Result: +10% Net Account Growth.

- With a 50% Win Rate: Result: +20% Net Account Growth.

The “7” ensures that you don’t need to be a market psychic to be profitable; you just need to be disciplined enough to let your winners run and cut your losers at the 3% mark.

3-5-7 vs. The 1% Institutional Standard

Professional fund managers frequently advocate for a 1% risk rule. While safer, the 1% rule is often impractical for retail traders with smaller accounts (under $50,000) who are trying to build wealth.

| Feature | 3-5-7 Rule | 1% Risk Rule |

| Growth Velocity | High (Aggressive Compounding) | Low (Capital Preservation) |

| Max Drawdown | 15–20% (Typical) | 5–8% (Typical) |

| Ideal For | Growth-phase retail accounts | Multi-million dollar funds |

| Tolerance | Requires high discipline | Requires high patience |

The 3-5-7 rule is the “sweet spot” for active traders. It is aggressive enough to see meaningful account growth but conservative enough to survive the inevitable “losing streaks” that occur in every trading career.

Strategic Adaptation Across Asset Classes

The 3-5-7 rule is a framework, but it must be calibrated based on the volatility of what you are trading.

1. The Crypto Adaptation (High Correlation)

In crypto, the “5% Total Risk” is the most important number. Because Bitcoin dictates the direction of 90% of altcoins, having five different altcoin trades is usually just one large, high-risk trade.

- Adjustment: Consider lowering the per-trade risk to 1.5% and keeping the 5% total cap to account for “Flash Crashes” that can skip past stop-loss orders.

2. The Options Adaptation (Theta Decay)

In options trading, 3% of the account can be lost very quickly due to time decay.

- Adjustment: Use the 3% rule as your hard exit on the contract price. If the premium of the option drops by an amount equal to 3% of your total account, the trade is dead.

3. The Swing Trading Adaptation (Gap Risk)

If you hold positions overnight, you face “Gap Risk”—where a stock opens significantly lower than it closed.

- Adjustment: If a stock is highly volatile, reduce the “3” to “2” to provide a buffer for slippage.

Why Traders Fail to Follow the Rule

The math of the 3-5-7 rule is simple. The execution is not. There are three psychological traps that lead traders to break these rules:

- The “Certainty” Trap: A trader sees a “guaranteed” setup and decides to risk 10% instead of 3%. When the trade fails, the emotional damage causes a spiral of revenge trading.

- The “Fear of Missing Out” (FOMO): A trader hits their 5% total exposure limit, but a new opportunity appears. They take the trade, over-leveraging their account just before a market reversal.

- The “Early Exit” Syndrome: A trader is up 4% on a trade. Fearing the profit will evaporate, they close the trade early, failing to reach the “7% benchmark.” Over time, their small wins cannot cover their 3% losses.

Step-by-Step Implementation Guide

This checklist is designed to be used before, during, and after the trading session. Its purpose is not speed—it’s consistency.

Before the Trading Day

- Confirm current account balance (risk must be recalculated daily)

- Define maximum per-trade risk (3% or less)

- Define maximum total exposure (5%)

- Identify correlated markets or sectors you plan to trade

Before Every Trade

Calculate position size using:

Position Size = Max Dollar Risk ÷ Risk Per Share

- Place stop-loss where the trade idea is invalid—not where size looks better

- Check total open risk after adding this trade. If it exceeds 5%, the trade is skipped

During the Trading Session

- Do not increase size after losses

- Do not add trades just because “nothing else is working”

- Monitor correlation: multiple positions moving together = hidden risk

After the Trading Day

- Record actual risk taken vs. planned risk

- Review whether exits followed the plan

- Note any emotional rule-breaking (this matters more than P&L)

Conclusion: Risk is the Only Edge

Most traders spend years looking for a “Holy Grail” indicator. They eventually realize that the Holy Grail doesn’t exist in a chart pattern—it exists in a spreadsheet.

The 3-5-7 rule is a tool for professionalizing your approach. It removes the need for “gut feelings” and replaces them with a mathematical certainty: if you keep your losses at 3%, your total exposure at 5%, and your wins at 7%, the math of compounding will eventually do the heavy lifting for you.

Trading is not about being right; it is about staying in the game long enough for the law of large numbers to work in your favor. The 3-5-7 rule ensures you are still standing when the “big move” finally happens.

Comparison Table: Rule Summary

| Component | Limit | Metric | Primary Function |

| Individual Risk | 3% | Account Equity | Prevents catastrophic single-trade failure. |

| Total Exposure | 5% | Combined Open Risk | Protects against market/sector correlation. |

| Profit Benchmark | 7%+ | Account Equity | Ensures positive expectancy and growth. |

| Risk-Reward | 2.33:1 | Ratio | Allows for a sub-50% win rate. |