Episode I: Trump’s tariffs announcement 1st of March, regarding steel and aluminum

Episode II : Many exceptions from tariffs (worth-noted Japan although an ally, was not exempt) and Trump’s goofy tweet

Episode III: Trump’s announcement for extra tariffs on 50B$ worth of Chinese exports and a verbal Chinese reaction from the mouth of China’s ambassador in USA

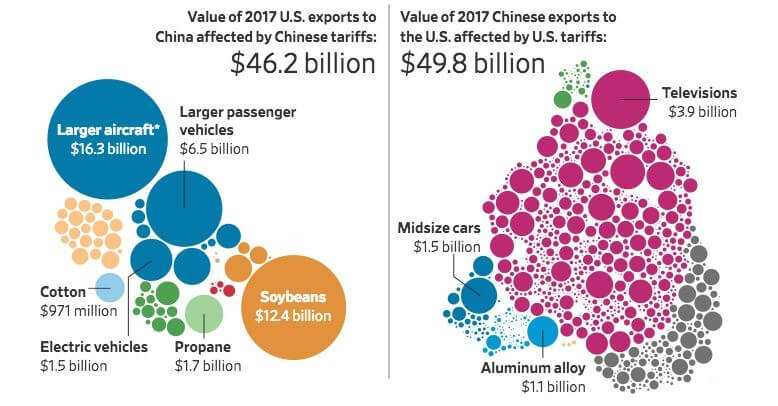

Episode IV: Wednesday’s China’s comprehensive list of tariffs on 50B$ worth of US exports, Trump’s counter response on Thursday (thinking of tripling the targeted tariffs to 150B$ worth of China’s exports), Kudlow’s comments downplaying the whole thing. Below is an enlightening chart, produced by Peterson Institute for International Economics that shows the -so far- targeted goods. It does not include the Trump’s Thursday’s announcement.

My readers have experienced much better forecasts than last’s week:

- Short positions on 131.70 EUR/JPY and 200DayMovingAverage where never triggered

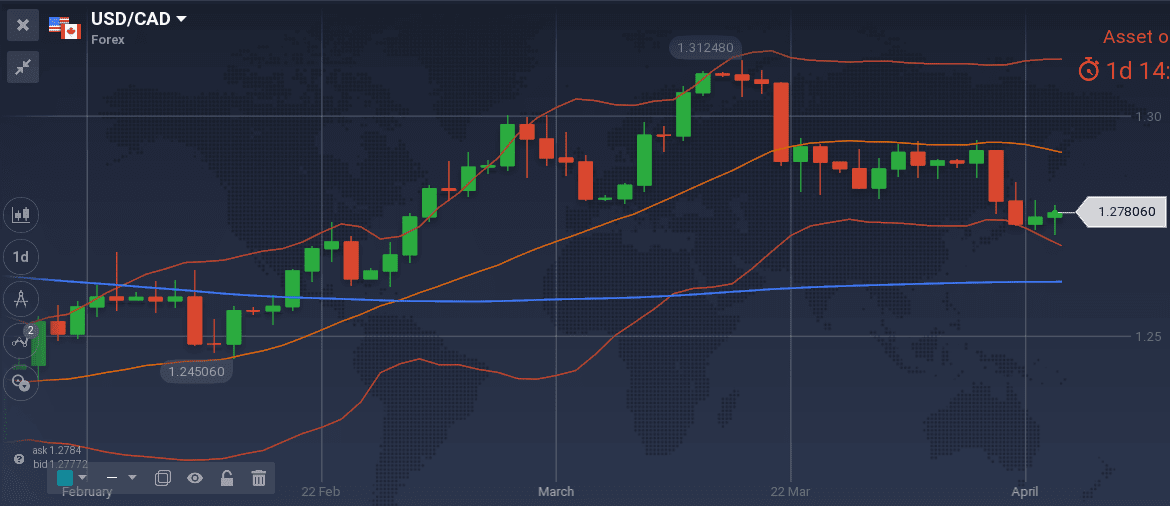

- Taking losses on my long USD/CAD position was the correct thing to do on the 4th April 14:30GMT when the US crude oil inventories where announced.

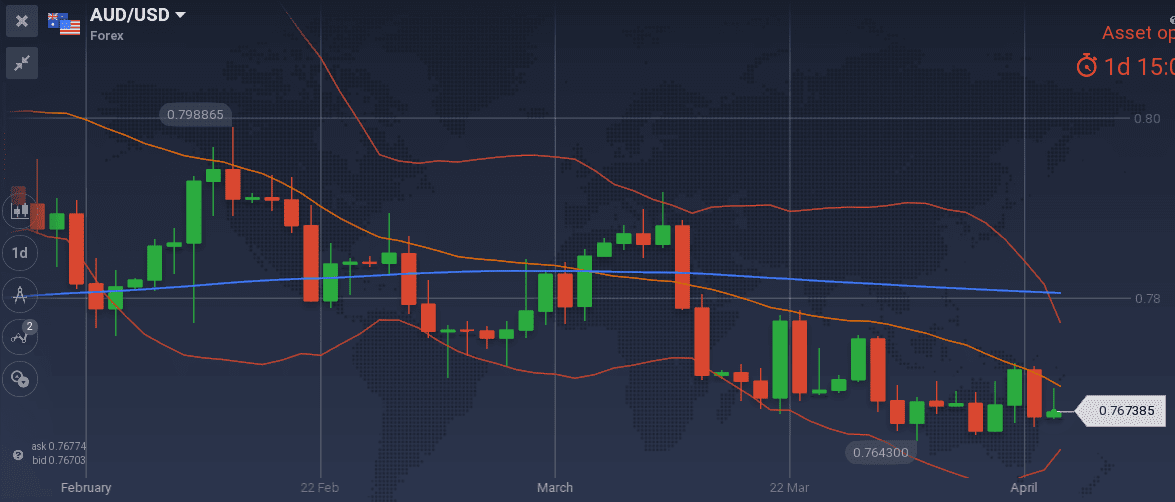

- AUD/USD indeed closed the week lower, but the 0.7820 level was never reached to add to my short position

- EUR/USD moved south as I was expecting.

- Proposed 1.3965 entry level for GBP/USD hit bull’s-eye, GBP/CAD position in the green, proposed entry levels for GBP/AUD and EUR/GBP where unfortunately never triggered.

Major last week’s events:

- We are heading to inter-Korean talks withing April and North Korea-USA talks in May. Note that military exercise of USA and South Korea was not postponed and remember the Ki’s (North Korea) visit in China, the content of which has not yet been published.

- Tariffs front: China announced a comprehensive list of tariffs via it’s Finance Minister Zhu Guangyao, Trump responded and Larry Kudlow, the director of the White House National Economic Council, downplayed and characterized the tariffs as just proposals.

- China’s defense minister visited Russia, Turkey is thinking of buying S-400 missiles from Russia and is presented to be on the same page with them regarding Syria, Russia is having missile tests near Latvia

- India hosted Japan and USA talks, ahead of Trump’s-Abe’s meeting later this month

- New attack in Münster Germany on Saturday with casualties. Cannot yet tell if it is a terrorist attack.

- On Monday we had the first close of US equities below the 200DayMovingAverage. The week ended with a new sell-off and a close just above the 200DayMovingAverage.

I keep betting on the high tension, high volatility, increasing inflation, increasing bond yields, decreasing equities scenario that favors haven currencies. I should note though that judging from 1Q18 move of the 10y US government bond yields (now at 2.81%) the 3.00% levels seem to be the ceiling for the year.

Major next week events:

- Monday’s Business Outlook Survey announcement by Bank of Canada

- Tuesday’s and Wednesday’s scheduled testimony of Mark Zuckerberg (Facebook) to US lawmakers

- Thursday’s OPEC monthly review of oil market

- Note the scheduled IMF meeting in two weeks’ time (20~22Apr)

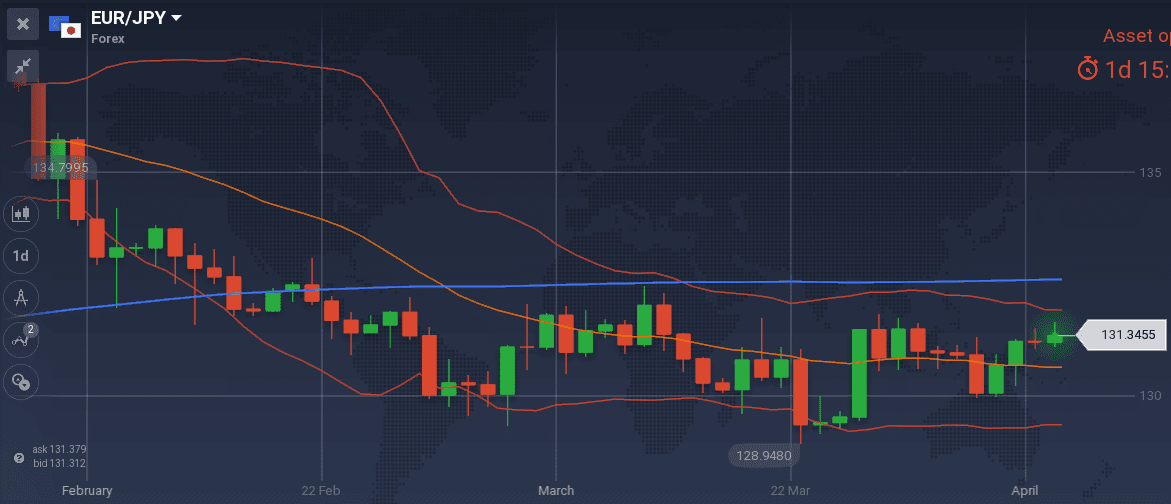

JPY

Last Tuesday’s 10Y Government Bond Auction (0.03% yield) weakened JPY. At the end of the week, the yield is back at 0.05% and JPY is strengthening. Both 131.70 level and the 200DayMovingAverage level were not triggered for me to build further my short position.

I keep my short EUR/JPY bias. Valid entry zone is 131.88 ~132.00

Snapshot:

- 0% GDP growth, all time low unemployment at 2.5%

- Inflation (excluding food-National core CPI) at 1.0% (vs 2.0% target) . Next release at 20Apr

- 05% 10y Bond yields vs BOJ’s target of 0.00% level

Strengths of JPY:

- decisiveness communicated by the Central Bank. Next meeting is scheduled within 26 April

- Trump’s tariff drama and new equity sell off favors JPY as it maintains it’s safe haven status

Weaknesses of JPY:

- Nothing to note

Watch:

- Monday’s 00.00 GMT Current Account. I am expecting a number above 1.8T JPY. Any number above the market’s consensus of 1.39T JPY helps my scenario.

- Next Monetary meeting on 26 April

CAD

Wednesday’s 14:30GMT US Crude oil inventories release, (actual number -4.6Mbarrels, below my stated threshold of 2.5Mb) made me close my long USD/CAD trade with a loss. Up until that time, China’s Finance Minister had already started episode IV of tariffs drama and my reasoning was that any strengthening of USD was already priced. The decision was correct for almost 21 hours. Thursday’s Trade balance release (at -2.7B CAD) and Friday’s new equity sell off were both new reasons for an increase of USD/CAD.

I will not offer an entry point to go long USD/CAD, as I keep on getting contradicting evidence. Yet, I should note that 1.2620 level would be very hard to be crossed.

Snapshot:

- Inflation at 2.2% (vs 1.0%~3.0% target range).

- GDP at 2.9% annual, 0.4% qoq, 10Y Government bonds yield (+6bps) at 2.15%

- Unemployment at 5.8% and expected to increase slightly until the end of the year. Yet last employment change was higher than anticipated

- Correlation of CAD with WTI and Brent price has decreased.

Strengths of USD/CAD, weakness of CAD:

- the latest GDP m/m low reading

- Last Thursday’s trade balance release of -2.7B CAD

- I continue correlating any increase of inflation with further weakening of CAD

- I still believe that no rate hike is considered for the next meeting on 18 of April.

Weaknesses of USD/CAD, strengths of CAD:

- US Crude oil inventories that are decreasing

- Last Friday’s strong employment change number (32.3K for February)

Watch:

- Business Outlook Survey release on Monday 14:30GMT, to see any clue on how the Central Bank is pricing the potential outcome of NAFTA talks.

- Next Monetary Meeting on 18 of April.

AUD

AUD/USD keeps on bouncing indecisively between a 50 pip narrower zone than the one I called (0.76~0.78) two weeks ago. Both market participants and the Central Bank (RBA) are waiting.

Nor the released Trade Balance, nor Tuesday’s RBA’s monetary decision to keep rates at 1.50% changed the picture. From RBA communication, worth noted:

- a remark on the rising short-term government yields across the globe that are not explained by FED’s tightening

- the fact that there was no mention on falling foreign demand for Australian housing, that was part of the 6th of Feb communication

- remarks on wages growth remained the same. Remember that next release of Australian wages is expected on the 16th of May. I believe that this is the only reading that could trigger an updated Central Bank’s view.

- worries about consumption, as household debt levels are high, and income is not growing as fast

I change my bias and search to go long in case 0.7550 is triggered.

Snapshot:

- Central bank ‘s interest rate is at 1.50% with no hike yet in this cycle.

- Inflation at 1.9% (vs 2.0~3.0% target), Unemployment at 5.6% and expected to decline

- GDP latest reading at 2.4% growth (2.8% was 2017 reading)

Strengths:

- Latest equity sell-off did not resulted in AUD decrease

Weaknesses:

- Latest declined GDP reading, declining terms of trade

- Latest increased unemployment reading at 5.6%

Watch:

- Wednesday’s 00:30 GMT Consumer Sentiment and Thursday’s 1:00GMT Inflation expectations. I want to check the validity of RBA’s worries on consumption. Lower readings give the green light for my long AUD/USD scenario.

- Next Monetary meeting on 4th of May. Note that markets are expecting the first-rate hike no earlier than the first half of 2019.

USD

I am keeping my long bias on USD. Last week was full of new events on the tariffs front, but when I read that Larry Kudlow, the director of the White House National Economic Council, downplayed the whole thing, I am crystallizing my view that (a)negotiations will stretch over many months, (b)any tariff to stand the critique of World Trade Organization needs to be backed by concrete arguments (c) tariffs are not meant to materialize before November midterm elections (d)the strengthening of USD is not in danger.

Snapshot:

- US economy growing at 2.9% (FED expects 2.7% in 2018), unemployment at 4.1% (FED expects to fall at 3.8% in 2018), inflation measured by PCE at 1.7% (FED expects 1.9% reading in 2018)

- We are counting 6 hikes of 25bps since Dec ’15, resulting to a current FED rate of 1.75%. FED’s dots are currently pointing to another 6 hikes by the end of 2019 (peak of 3.25% in this cycle) and FED’s view of long run rate remains at 2.75%~3.00%

Strengths of USD:

- strong macroeconomic announcements and yields of Government bonds (now at 2.77%. Worth noted that 3.00% seems to be the ceiling for 2018)

- weakening of US equities.

Weaknesses of USD:

- Tariffs drama is proving to be the market mover of 2018. So far, the higher the tariffs and higher probability to be imposed, the weaker the outlook for USD

Watch:

- Wednesday’s 17:00 GMT 10y Government Bond auction. Last auctioned yield was 2.89%. Any number above it, strengthens my scenario

- Wednesday’s 18:00 GMT release of latest FED’s minutes of meeting

- Friday’s 14:00 GMT Consumers Sentiment. There are little chances of a new record high reading, but if a new record happens, it would strengthen my scenario

- Next Monetary Meeting on 2nd of May

EUR

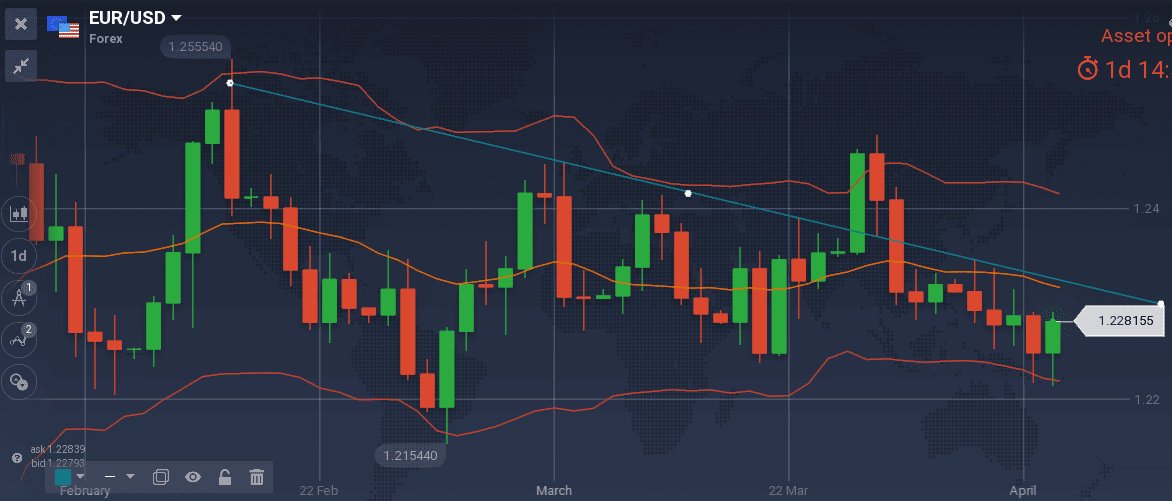

I am keeping my short bias towards EUR/USD and still playing the divergence scenario.

My proposed rule of thumb is that EUR/USD should strengthen whenever there is a new episode of the tariffs serial and weaken whenever there is an equity sell-off. On Friday we had a big sell-off, no more news in the tariff front, yet the pair strengthened. Technically we are in the same spot as the close of 23 March, as EUR/USD is approaching the drawn downtrend line and S&P500 closed near it’s 200DayMovingAverage.

Nice zone to enter short is 1.2410~1.2420

Snapshot:

- European’s Economy is doing well. Actual GDP growth at 2.7%, unemployment decreased to 8.5%, core CPI inflation (watched by ECB) at 1.0%. I am confident with my view that the rosy picture was already priced at the 1.25 peak

Strengths of EUR/USD:

- tariff drama strengthens the pair. Yet, there is a great probability that all of the tariff talking will remain verbal and will not materialize.

- Destroyed double top formation at 1.25 level and bridged downtrend

Weaknesses:

- divergence of EU’s and USA’s economy. Note that both Spanish and French Bond’s auctions of last week, resulted in lower yields. Spanish 10y Bonds at 1.15% (-21bps from previous auction), French 10y Bonds at 0.74% (-16bps) while the 10y US bonds yield 2.77% (+1bps from previous week)

- core CPI (inflation index watches by ECB) unchanged at 1.0%

- latest PMI readings slightly decreased

Watch:

- Monday’s 6:00GMT German Trade Balance for February. A reading below 23.1B EUR is within my scenario

- Friday’s 9:00GMT European Trade Balance for Feb18. A reading below 20.2B EUR is within my scenario

- Next ECB’s Monetary meeting scheduled for 14 June.

GBP

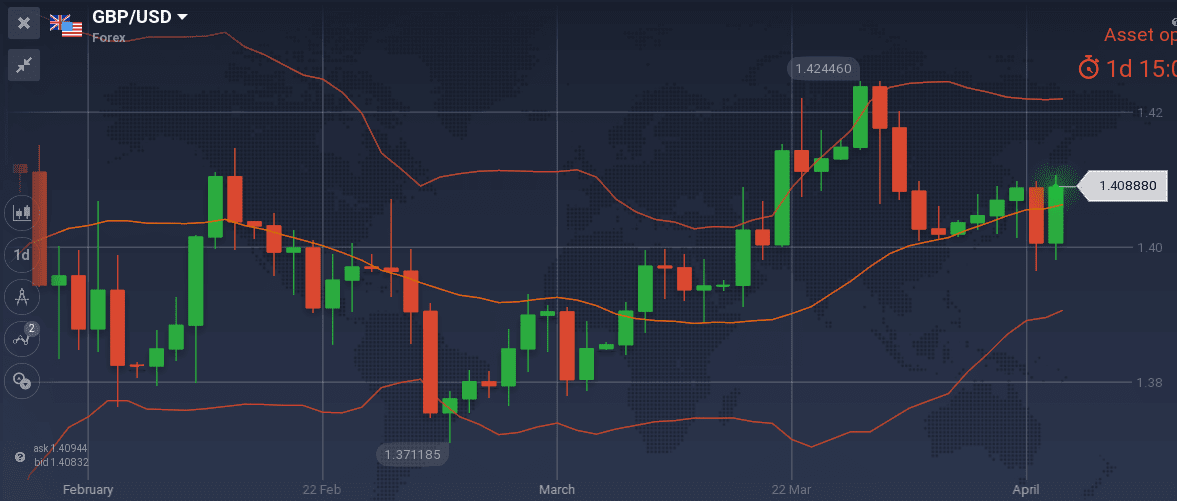

I keep my long bias on GBP and note down the levels I am thinking of entering the market

- long GBP/USD at 1.4005

- long GBP/CAD at 1.7810

- long GBP/AUD at 1.8090, 1.8000 and 1.7955 (same proposed levels as previous week)

- short EUR/GBP at 0.8830 and 0.8801 (same proposed levels as previous week)

Snapshot:

- 4% GDP growth, 4.3% unemployment(record low) and 2.70% inflation (only major economy with higher inflation than the targeted 2%, but finally now it is decreasing), 10y Government bonds at 1.40%

- Current BOE rate at 0.50%, second rate hike on the 10th of May is turning very probable.

Strengths:

- Macro announcements are showing that the economy is strong, like the improved Current Account, the increased revision of business investments

Weaknesses:

- decreased reading of M4 Money Supply m/m at -0,3%

- decreased construction and service PMI

Watch:

- Wednesday’s 8:30GMT Goods trade balance. Any number above -12.3B GΒP strengthens my scenario

- Next Monetary meeting on 10th of May