The dollar has recently fallen to long term lows on shifting central bank outlook, but the pendulum is about to swing the other direction. The dollar’s fall was due to the combination of improving/better than expected data from the EU, the UK and Japan mixed with softening outlook for FOMC rate hikes. The problem for traders, that was then this is now.

Over the past two week’s we’ve had policy statements from the BOJ and ECB that did not live up to expectations. The BOJ was expected to make some indication of support for the economy with a hint of when they may begin taper/tightening. What they did was quite the opposite; reiterating their dovish stance and pledging current QE operations would continue into 2019 at least. The ECB was likewise expected to make some indication of hawkishness and they did, it just wasn’t anything near what the market wanted and came with the caveat the bank plans to keep current QE into 2019 with a possibility of increasing it should they need.

The FOMC, also over the past weeks and months, has seen a steady decline in outlook. Yes, the bank is still expected to raise rates this year, possibly three times, but that outlook has been diminishing on tepid data and persistently low inflation. The combination of strengthening ECB/BOJ/BOE outlook and weakening FOMC outlook is what sent the dollar to new lows… but that is all about to change.

The failure of the ECB and BOJ to live up to expectations has set their respective currencies up for a fall versus the dollar. With little reason to expect aggressive ECB or BOJ action and every reason to expect FOMC rate hikes the odds of a dollar advance are growing. Monday’s Income and Spending data, including the ever important PCE price index, keeps the FOMC on track with a chance of stepping up the timeline, a move that would put the committee’s policy in divergence once again.

While the FOMC meeting is off utmost importance this week there are also quite a few economic reports that could help or hinder a dollar advance. On the manufacturing front there are 3 important reads including Chicago PMI, ISM Manufacturing Index and Factory Orders. On the employment front look out for the ADP report, the NFP, Unemployment and Average Hourly Earnings. It is accepted that labor markets are tight, so the most important data may be the average earnings. They have been rising at a 2.5% annualized pace over the past 2 years and are underpinning core inflation.

- FOMC policy statement to be released Wednesday at 2PM and is likely to spark big moves in dollar denominated pairs.

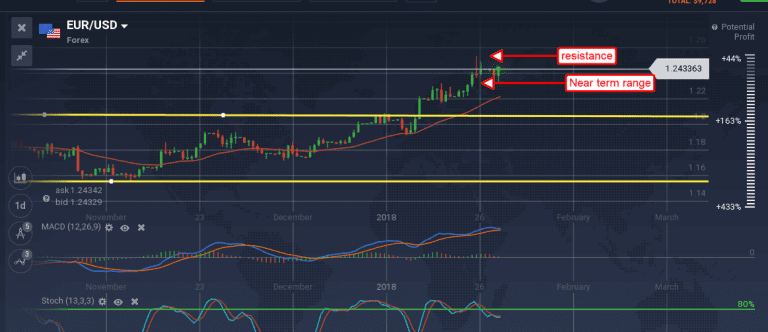

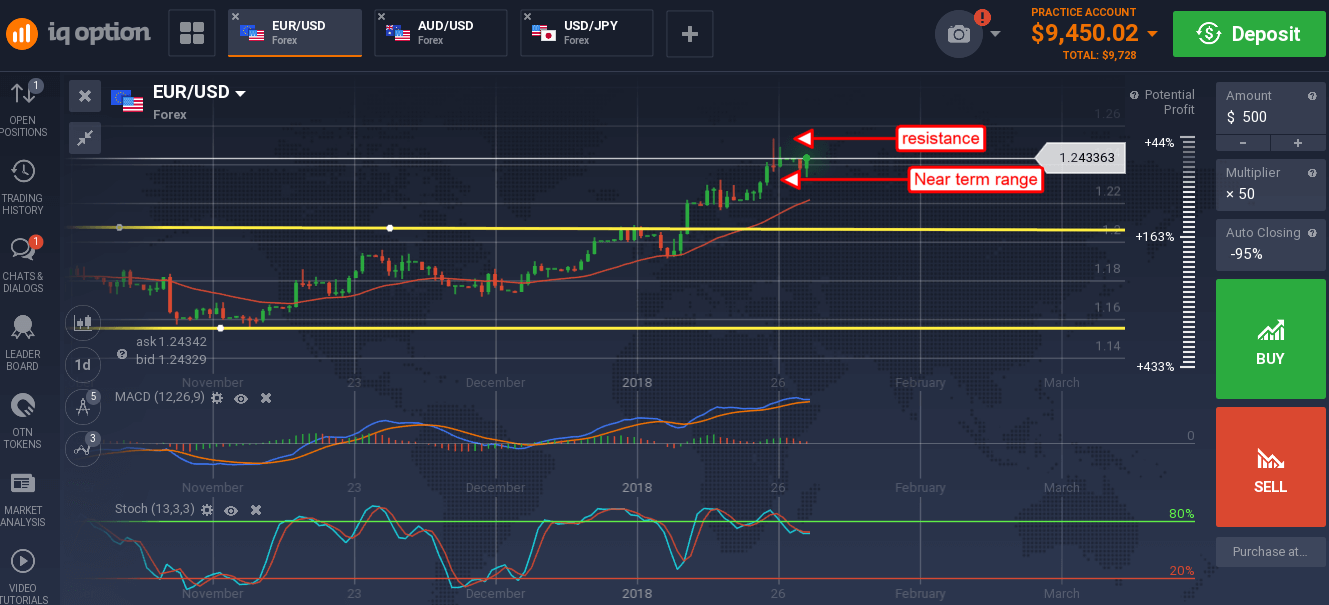

The EUR/USD is in consolidation just below long-term highs. This move, the consolidation, was sparked last week with the ECB statement/Trump remarks about a stronger dollar. He says he wants one, and that it is good for the US. The pair is now sitting on near term support of 1.2400 with a change of sideways movement over the Tuesday/Wednesday trading session.

The indicators are mixed, consistent with consolidation, range bound trading and a possible peak within the past month’s up trend. A move up may face resistance at 1.2540, a break above that would be bullish long term. A break below support at 1.2400 would be bearish with targets near 1.2300, 1.2200 and 1.2100.

The USD/JPY moved lower in the early Tuesday session and looks like it may move down to test longer term support at 107.50. The indicators are bearish and support such a move but are also divergent from current lows suggesting the down trend is coming to an end. A dip to support may be bearish but is not tradable until support is broken.

A bounce from current levels or support in the 107/108 range would be bullish with target near the top of the range at 113.50. The FOMC may not spark reversal in the dollar but it is likely to spark volatility in both the EUR/USD and USD/JPY.