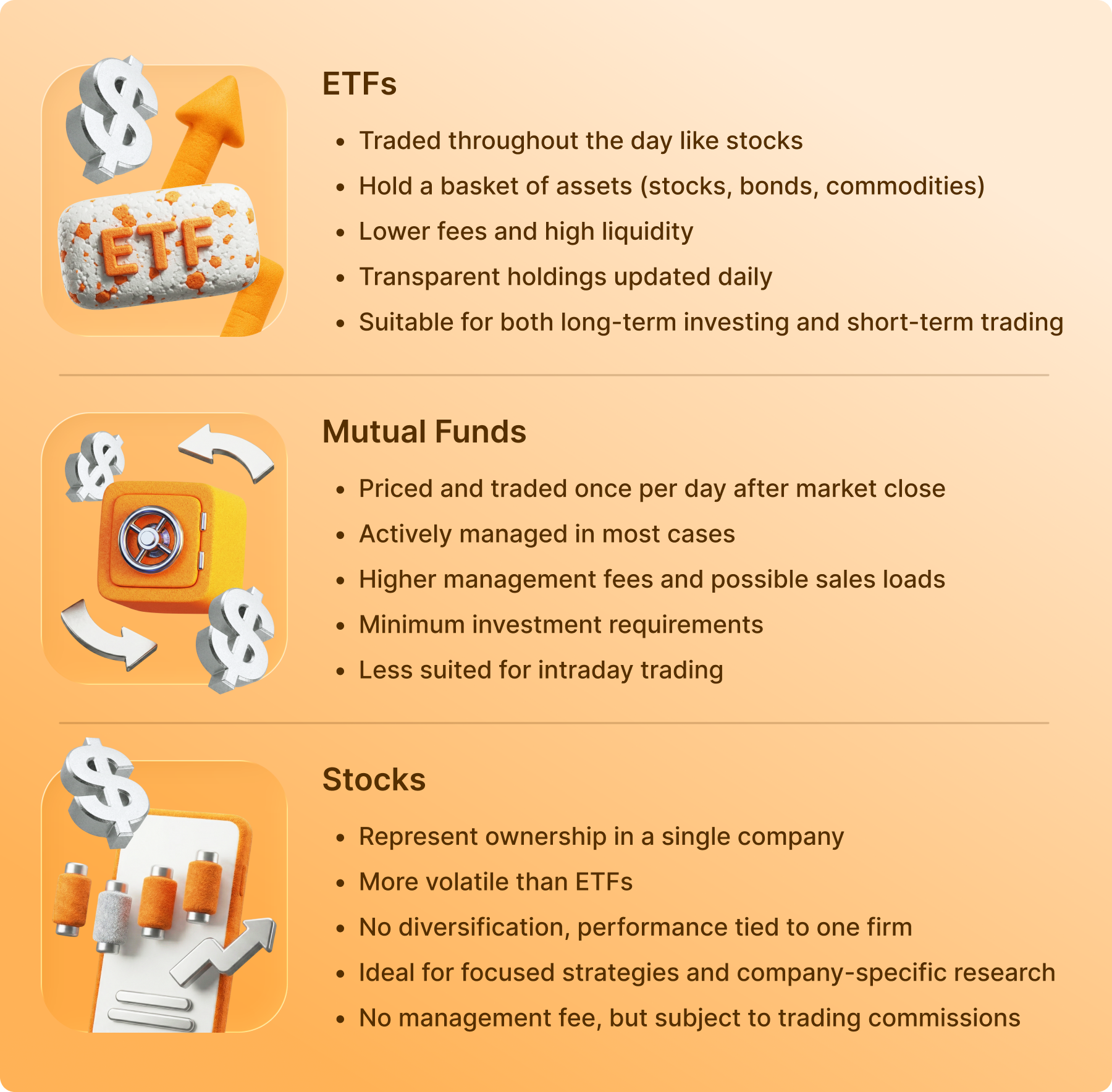

The primary difference between an ETF (Exchange-Traded Fund) and a mutual fund is how they are traded: ETFs trade like stocks throughout the day at real-time market prices, while mutual funds are only bought and sold once per day after the market closes at a fixed price called the Net Asset Value (NAV). Beyond the “clock,” ETFs are generally more tax-efficient and have lower overhead costs because they are mostly passively managed to follow an index. Mutual funds, meanwhile, are the traditional heavyweights of the retirement world, often led by professional managers who actively try to beat market averages.

In early 2026, the choice between these two has never been more relevant. We are currently witnessing a massive “migration” of capital, as active ETFs have captured a record 40% of all new investment flows in January 2026 alone, signaling a shift away from old-school mutual fund structures.

What Is the Difference Between ETF and Mutual Fund?

If you’ve ever looked at your brokerage app, you’ve likely seen a soup of three-to-five-letter tickers. At their core, both ETFs and mutual funds are “wrappers.” They are just baskets that hold stuff: stocks, bonds, gold or even other funds. Instead of you going out and buying 500 individual stocks to own the S&P 500, you buy one share of a fund that does it for you.

However, the way you interact with that basket (and how the IRS looks at it) is where things get interesting.

The “Speedboat” vs. The “Bus”

Think of an ETF like a speedboat. You can hop on and off whenever you want while the sun is up. If you see a storm coming at 11:15 AM, you can dock it immediately and get your cash. The price you get is the exact market price at that second.

A Mutual Fund is more like a city bus. It has a set schedule. You can get on at any time during the day, but the bus only reaches the final destination (the “price”) at 4:00 PM when the market closes. Everyone on the bus that day pays the exact same “fare,” regardless of whether they hopped on at 9:00 AM or 3:55 PM.

Trading and Liquidity: The 11:15 AM Trade vs. The 4:00 PM Wait

In the 2026 market, volatility can strike in minutes. This is where the trading structural difference becomes a tactical advantage or a frustrating bottleneck.

Real-Time Pricing (ETFs)

Because ETFs trade on an exchange (like the NYSE or Nasdaq), their price fluctuates every second. This allows for sophisticated order types:

- Limit Orders: “I only want to buy this if the price drops to $100.”

- Stop-Losses: “Sell my shares automatically if the price hits $95 to protect my gains.”

- Short Selling: You can actually bet against an ETF if you think a sector is going down.

End-of-Day Pricing (Mutual Funds)

Mutual funds don’t have “prices” in the traditional sense during the day. They have a Net Asset Value (NAV). The fund manager looks at the value of everything the fund owns at 4:00 PM, subtracts the fund’s expenses, and divides it by the number of shares. That is the price you get. If you place a “sell” order at 10:00 AM, you won’t know your exit price until dinner time.

The Invisible Tax Bill: Why ETFs Usually Win at Tax Time

One of the biggest “gotchas” in investing is receiving a tax bill for a fund that actually lost money during the year. This happens to mutual fund owners all the time, but rarely to ETF owners.

The Mutual Fund “Tax Trap”

When a mutual fund manager needs to pay out an investor who is leaving the fund, they often have to sell stocks within the portfolio to raise cash. If those stocks have gone up since the manager bought them, it triggers a capital gains tax.

The kicker? You have to pay a portion of that tax even if you didn’t sell a single share of your own. In 2024, nearly 43% of equity mutual funds sent out taxable capital gains, while only about 5% of ETFs did the same.

The ETF “In-Kind” Magic

ETFs use a clever loophole called “in-kind redemptions.” Instead of selling stocks for cash (which is a taxable event), the ETF manager swaps “baskets” of stocks with institutional players (Authorized Participants) for ETF shares. Because no cash changed hands, the IRS doesn’t see it as a sale. You only pay taxes when you decide to sell your shares for a profit.

Creation and Redemption: How the “Magic” Happens

This is the technical “plumbing” that explains why ETFs are so efficient. It involves a character called the Authorized Participant (AP).

- Creation: When demand for an ETF goes up, the AP buys a bunch of the underlying stocks (like Apple, Tesla, etc.) and gives them to the ETF provider. In exchange, the provider gives the AP a block of ETF shares.

- Redemption: When people are selling the ETF, the process goes in reverse. The AP gives the ETF shares back to the provider and gets the actual stocks in return.

This process keeps the ETF price very close to the value of the stocks it owns. It also keeps the fund from having to hold big piles of “uninvested cash” to pay out withdrawals—a problem called “cash drag” that often slows down mutual fund returns.

5. Total Cost of Ownership: Expense Ratios and “Hidden” Fees

In 2026, the mantra “fees matter” has never been truer. Over a 30-year career, a 1% difference in fees can cost you hundreds of thousands of dollars in lost compounded growth.

Explicit Costs (The Expense Ratio)

- ETFs: Mostly passive, meaning a computer does the work. These are dirt cheap. In 2026, some S&P 500 ETFs have expense ratios as low as 0.03% ($3 for every $10,000 invested).

- Mutual Funds: Often active, meaning a human in a suit is trying to pick winners. This costs more. Average active equity mutual funds still hover around 0.90% to 1.10%.

Implicit Costs (The Spreads)

Don’t be fooled; ETFs have a hidden cost called the Bid-Ask Spread. This is the difference between what you pay to buy and what you get when you sell. For popular ETFs, this is pennies. For niche, low-volume ETFs, it can be a significant “entry fee” that mutual funds don’t have.

Total Cost Formula:

Investor Cost = (Expense Ratio * Balance) + Bid-Ask Spreads + Taxes Paid

7. Main Risks: What Could Go Wrong?

No investment is a “sure thing.” Both “wrappers” carry risks that can catch a beginner off guard.

| Risk Type | ETF Risk Profile | Mutual Fund Risk Profile |

| Market Risk | If the market drops, you lose money. | If the market drops, you lose money. |

| Tracking Error | High risk that the fund misses its index performance. | Lower (since they aren’t always tracking an index). |

| Liquidity Risk | High in a panic; you might sell for less than the “true” value. | Low; the fund must pay you the NAV at the end of the day. |

| Manager Risk | Low (mostly computer-led). | High (you’re betting on the manager’s skill). |

8. 2026 Market Shifts: The Rise of the Active ETF

The biggest trend we’re seeing in 2026 is the “hybrid” child: the Active ETF. This takes the brain of a mutual fund manager and puts it inside the “tax-efficient, tradable” skin of an ETF.

In 2025, over 80% of new ETF launches were actively managed. This is disrupting the old guard because it offers the potential to beat the market without the heavy tax bill at the end of the year.

Expert Insight: “We’re seeing a fundamental shift in how people view their portfolios,” says a lead analyst at a top 2026 brokerage. “The ‘active vs. passive’ debate is dying. Now, it’s just about choosing the best ‘wrapper’ for the strategy you want.”

9. Popularity Trends: Dinosaurs vs. Speedboats

By early 2026, the numbers are clear:

- Inflows: Long-term index funds (mostly ETFs) saw an inflow of $162 billion in December 2025 alone.

- Outflows: Active mutual funds saw a net outflow of $86 billion in that same month.

Investors are voting with their wallets. They want lower fees, better transparency (ETFs disclose their holdings every day, while mutual funds often only do so once a quarter), and the ability to trade whenever they want.

Summary and Next Steps

Choosing between an ETF and a mutual fund isn’t about which one makes more money—they could both hold the exact same stocks. It’s about cost, taxes, and control.

- Go with an ETF if you want the lowest fees, the most tax efficiency, and the ability to sell in the middle of a lunch break.

- Go with a Mutual Fund if you want a professional to pick your stocks, you’re using an employer plan, or you want a simple, automated deduction from your paycheck every month.