Every four months, a handful of tech companies move trillions of dollars in the market within hours. Alphabet, Microsoft, Apple, Nvidia, Amazon, Meta, and Tesla together control a huge portion of the Nasdaq and S&P 500 — when they report earnings, entire sectors move, from AI to crypto.

The April–May earnings cycle is where traders learn whether the AI boom, cloud growth, and consumer demand are still accelerating — or starting to slow.

Let’s break down the math behind Big Tech earnings season, explore what Q2 2026 earnings might look like, and how traders can use this information.

The Strategic Importance of Big Tech Earnings

So, because Big Tech dominates major indices like the Nasdaq, their earnings often determine short-term market direction. A strong report from one company can trigger rallies across related sectors such as:

- cloud infrastructure and AI computing

- electronics and online services

- semiconductors and data centers

- digital advertising

Metrics Investors Monitor During Earnings Season:

- Revenue growth

- Earnings per share (EPS)

- Segment performance (cloud, advertising, AI, hardware)

- Forward guidance for the next quarter

Big tech earnings also influence related industries — from semiconductor manufacturers and data-center operators to consumer retail and logistics companies.

👉 For a deeper explanation of how fiscal quarters and corporate reporting cycles work, read our guide on the structure behind earnings announcements.

Why Big Tech Earnings Matter More in 2026

This earnings season is especially important because several major trends are shaping the tech sector.

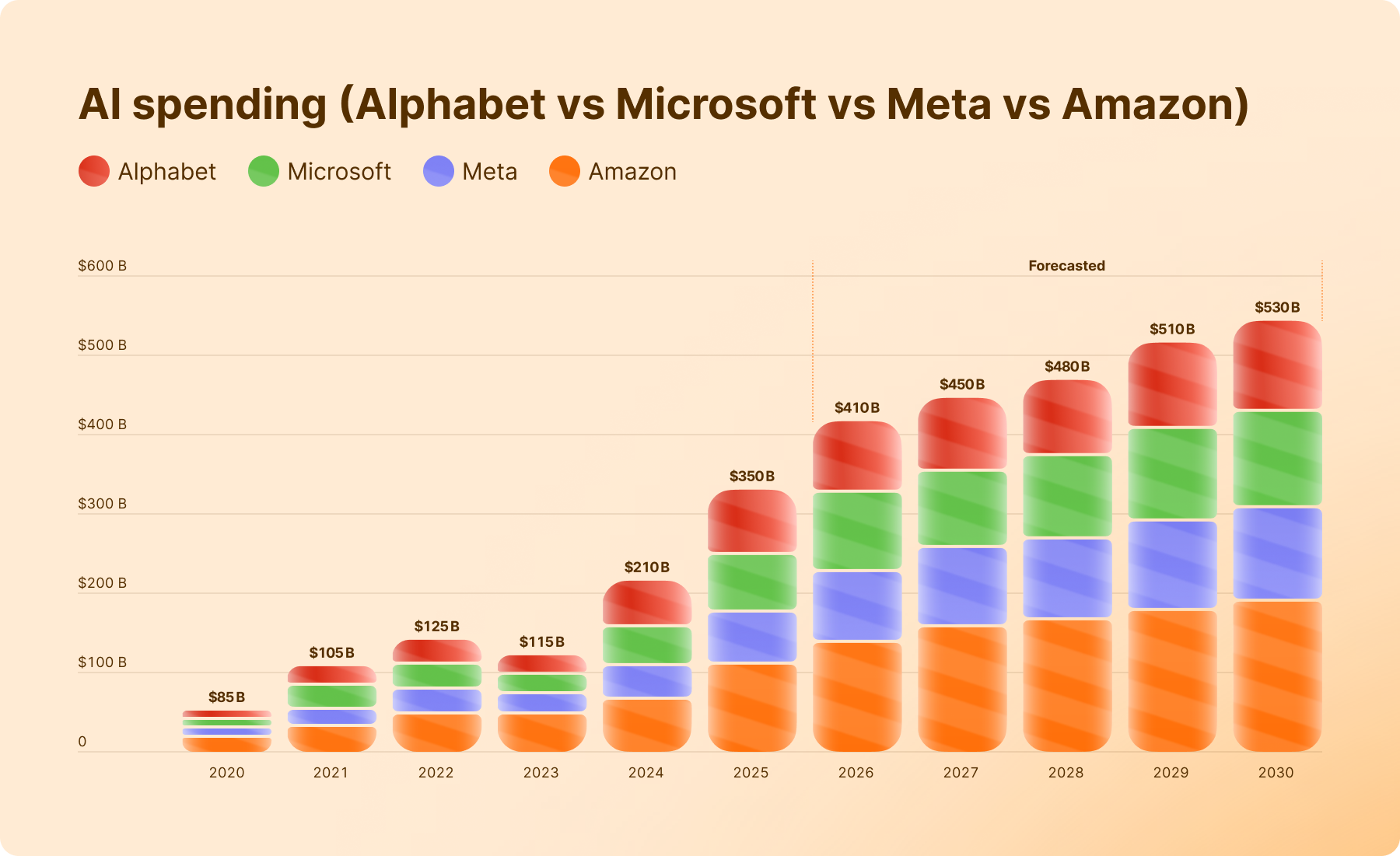

- AI investment boom — Companies are spending billions on chips, data centers, and AI infrastructure. But at the same time, some analysts are starting to question whether the market is overestimating the speed of AI growth, raising speculation about a potential AI bubble. Earnings reports will help investors see whether the massive spending is already translating into real revenue.

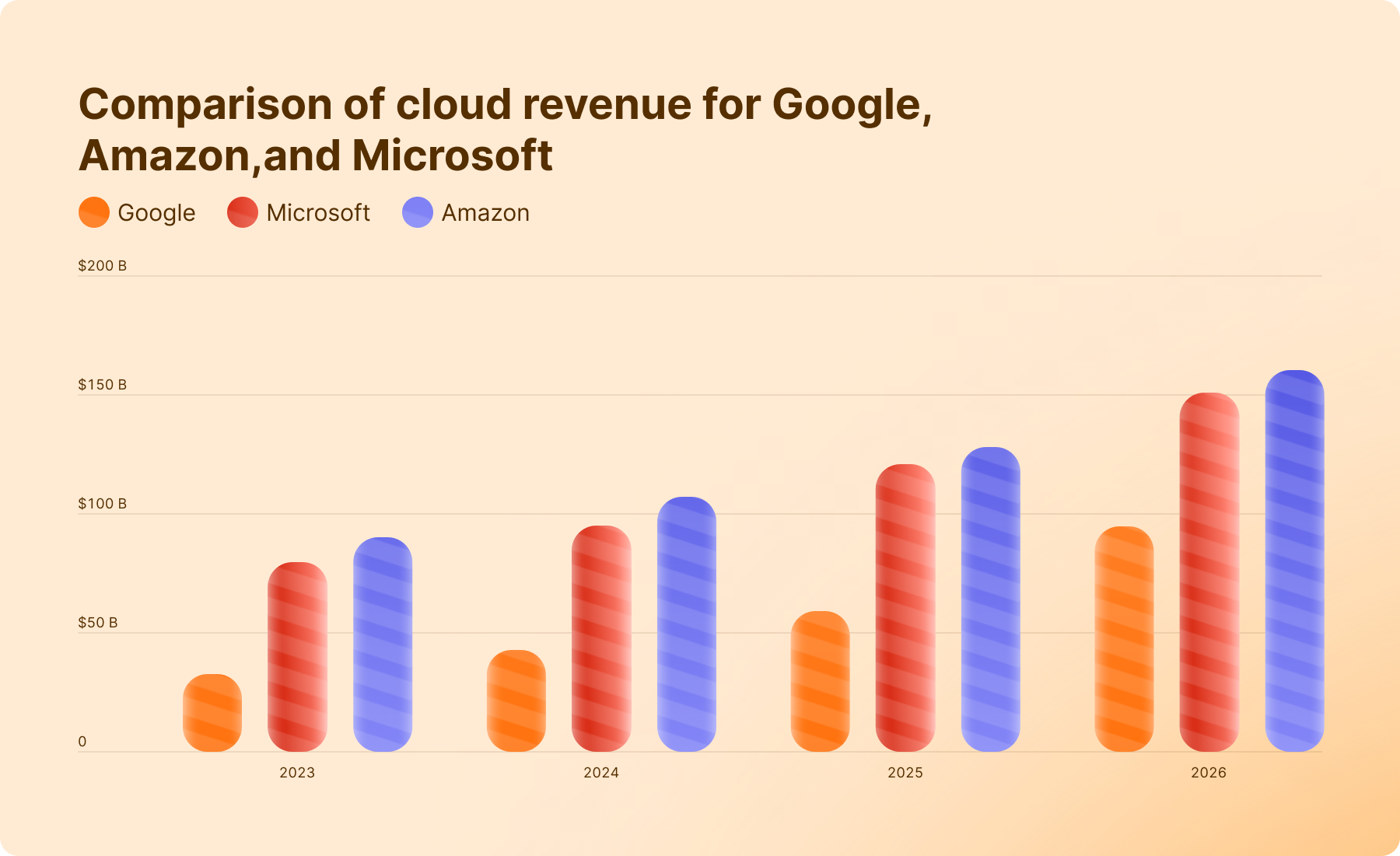

- Hyperscaler capital spending from companies like Microsoft, Amazon, and Alphabet. Their investment plans often signal future demand for AI hardware and cloud services.

- Interest rates remain an important macro factor, as higher borrowing costs can pressure high-growth technology stocks.

- Companies like Apple, Amazon, and Tesla provide insight into global consumer demand, helping investors understand whether spending on technology and online services is strengthening or slowing.

What’s in It for Traders?

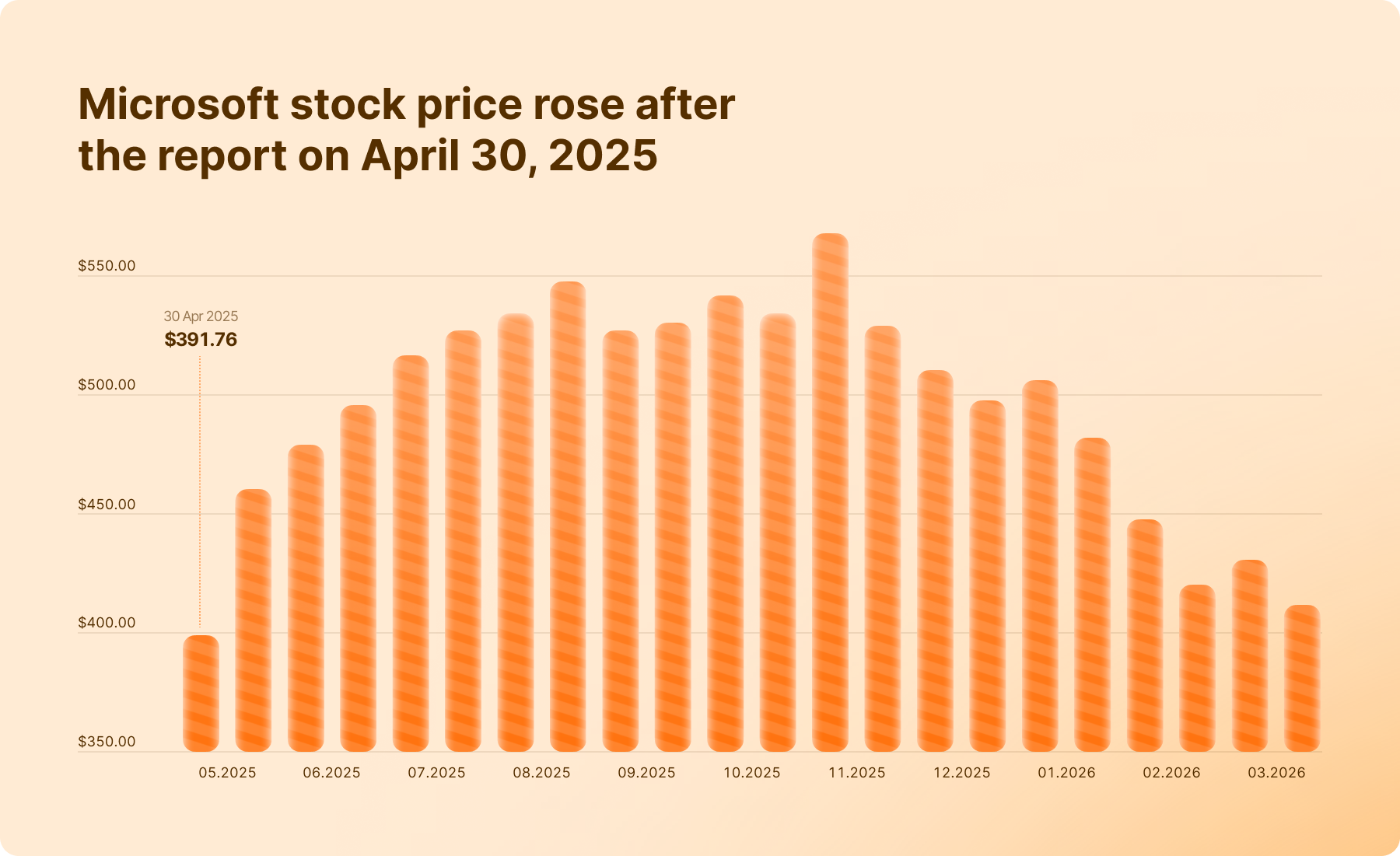

Historically, earnings that exceed expectations tend to trigger bullish price reactions — though not always. For instance, Google and Microsoft both reported strong earnings in 2025, which contributed to bullish sentiment after the announcements.

Big Tech Companies’ Earnings Projections for April–May 2026

Let’s analyze the key metrics to watch for companies like Alphabet, Microsoft, Apple, Nvidia, Meta, Tesla, and Amazon.

Alphabet Inc. (GOOGL): What to Watch

The forecast for Alphabet (Google) is set at ~40% YoY, and the results often set the tone for the entire technology sector.

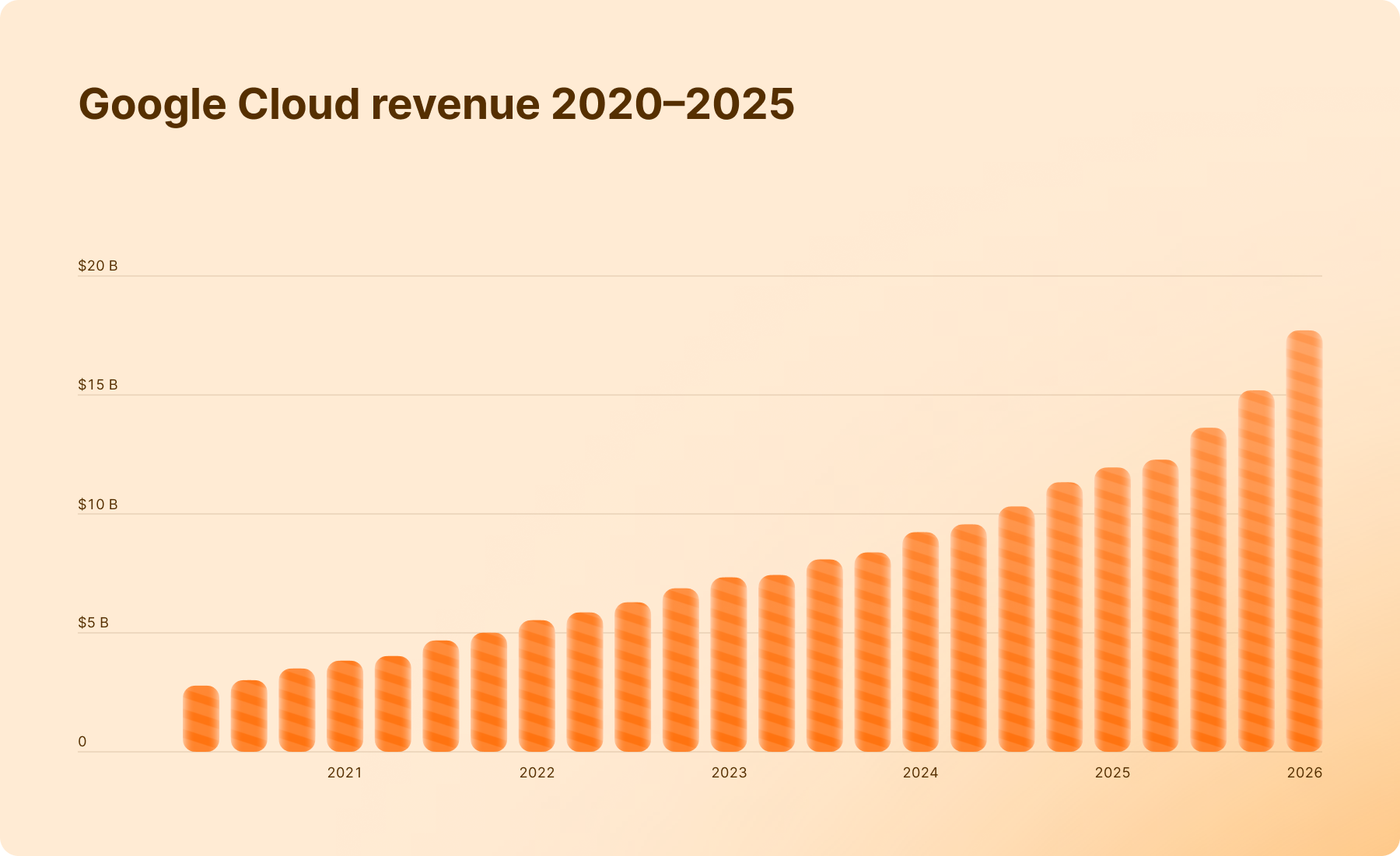

- Google Cloud revenue growth

Analysts currently expect Google Cloud growth around 25% year-over-year.

- >40% YoY growth (EPS >2.55) → Strongly Bullish: Signals that Google is successfully converting its massive AI backlog into revenue, potentially triggering a sector-wide rally in AI infrastructure stocks such as Nvidia and AMD.

- 35%–39% growth (EPS ~2.40) → Neutral: Viewed as a healthy, sustainable “digestion” period following the Q4 sprint.

- <30% growth (EPS <2.25) → Bearish: Would suggest that despite the high CapEx, Google is struggling to monetize its Gemini 3 integrations at scale.

- Advertising revenue (Search and YouTube)

In Q2 2026, investors will focus on whether AI-powered search improves or weakens ad click-through rates.

Key Metric: Total Advertising Revenue (target: $75B–$78B).

Market reaction: Strong ad growth typically drives the first after-hours price move. Continued growth in YouTube Shorts monetization alongside AI-powered Search would signal that Alphabet is successfully defending its position against AI competitors like Perplexity and OpenAI.

- AI infrastructure investment

Alphabet plans $175B–$185B in CapEx for 2026, with about 60% for AI servers (GPUs/TPUs) and 40% for new data centers.

Impact on partners: Bullish for Nvidia and AMD, signaling continued demand for AI chips.

Impact on Alphabet stock:

- High CapEx + strong cloud growth → Bullish

- High CapEx + weak cloud growth → Bearish

Microsoft Corp. (MSFT) — What to Watch

Microsoft’s earnings report is equally important because of its leadership in enterprise cloud services and AI software integration. Here’s what we’re watching:

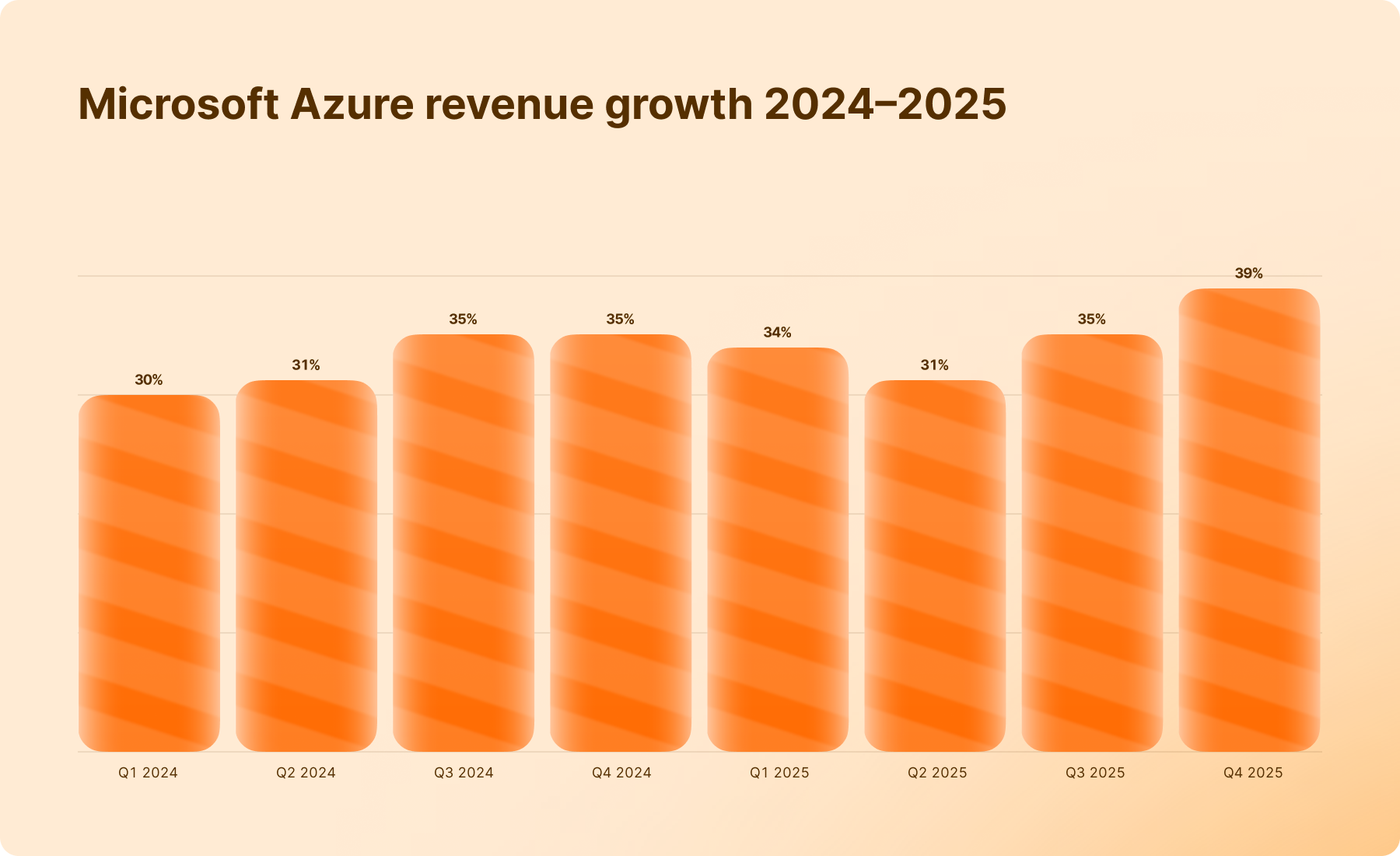

- Azure cloud growth

Azure’s growth rate reflects demand for enterprise cloud infrastructure and AI computing power. Analysts expect growth around 37-38% year-over-year.

- ≥40% YoY growth (EPS ≥4.15) → Bullish: Shows Azure is turning huge AI investments into strong revenue growth.

- 37–39% growth (EPS ~4.07) → Neutral: Around current expectations; suggests steady growth at Microsoft’s scale.

- <35% growth (EPS <3.95) → Bearish: May worry investors that AI spending is rising faster than revenue.

- AI contribution

Microsoft’s partnership with OpenAI and the integration of AI tools across its ecosystem are major drivers of market sentiment.

- The “Maia” Factor

Investors will also be watching the rollout of Maia 200, Microsoft’s second-generation in-house AI chip. Success here would reduce Microsoft’s reliance on Nvidia, potentially expanding Azure’s gross margins which have been under pressure due to high hardware costs.

- Forward guidance

If Microsoft upgrades its outlook for the next quarter, it could push technology indices and AI-related stocks higher.

Amazon.com Inc. (AMZN) — What to Watch

Amazon enters Q2 2026 under a cloud of investor skepticism following its massive $200 billion capital expenditure announcement. The market is no longer asking if Amazon can grow; it’s asking if the return on AI investment will ever outweigh the staggering cost of building it.

- AWS growth

Amazon Web Services growth sped up to 24% YoY at the end of 2025. Now Amazon needs to show that AI demand is very strong and limited by supply, not slowing down because customers are buying less.

- ≥28% YoY growth (EPS ≥1.75) → bullish reaction

- ≈24–27% growth (EPS ≈1.63) → neutral reaction

- <22% growth (EPS <1.55) → bearish reaction

- Retail and e-commerce sales

Retail Ad Revenue >$18 Billion will be considered bullish signal; <$15 Billion — bearish signal.

- AI infrastructure investment

Higher spending is no longer a “lift” for the sector; it’s an expectation.

- Impact on Semi Stocks: Any confirmation that Amazon is shifting more toward its proprietary Trainium 3 chips could actually be bearish for Nvidia, as it signals a move toward self-sufficiency.

- The “DOGE” Overhang: Investors are also watching for any impact from the Department of Government Efficiency (DOGE) on AWS GovCloud contracts, which have historically been a stable revenue floor.

Tesla Inc. (TSLA) — What to Watch

Tesla’s report provides insight into the electric vehicle market and emerging technologies.

- Vehicle deliveries and production outlook

Analysts currently expect ~3–5% year-over-year growth.

- ≥5% YoY growth (EPS ≥$0.45) → Bullish: Shows Tesla sales are stabilizing.

- 0–3% YoY growth (EPS ~$0.41) → Neutral: Growth is slow but stable.

- Negative YoY growth (EPS <$0.38) → Bearish: Signals weaker EV demand and more pressure on Tesla’s AI and robotaxi plans.

- Automotive gross margin

Margins are a key metric for Tesla.

- Above 18% → positive sign of stable profitability.

- Near 15% → bearish signal that Tesla may be losing its cost advantage to competitors.

- Autonomous driving and AI initiatives

AI updates are now a key driver of Tesla’s stock. Watch for:

- Cybercab production timeline and Robotaxi expansion.

- Optimus robot updates — factory testing news could boost the stock even if car sales disappoint.

Apple Inc. (AAPL) — What to Watch

While companies like Amazon and Google are spending heavily on AI infrastructure, Apple is using its 2.5 billion active devices to introduce privacy-focused AI without massive spending.

Because Apple has one of the largest market capitalizations in the world, its earnings can significantly impact major stock indices.

- iPhone 17 & The “Edge AI” Cycle

The iPhone is still Apple’s main product, but investors are now watching the average selling price (ASP). The success of the iPhone 17 Pro shows that customers are willing to pay more for phones with on-device AI features.

- ≥15% YoY growth (EPS ≥ $2.05) → Bullish: Shows strong demand for Apple devices and AI features.

- ~10–14% growth (EPS ~ $1.92) → Neutral: Growth is in line with expectations.

- <8% growth (EPS < $1.85) → Bearish: Signals weaker demand or stronger competition, especially in China

- Services segment growth

Watch the adoption of Apple Intelligence Pro. Analysts expect Services growth above 14% to make up for slower hardware sales.

- China market performance

Despite earlier concerns in 2025, Apple entered 2026 as the top smartphone brand in China. Investors will watch whether strong sales continue as Apple competes with Huawei’s new Mate 80 series.

- AI integration

The focus is now on Siri 2.0 (Campos). Investors will watch how many users subscribe to Siri Pro.

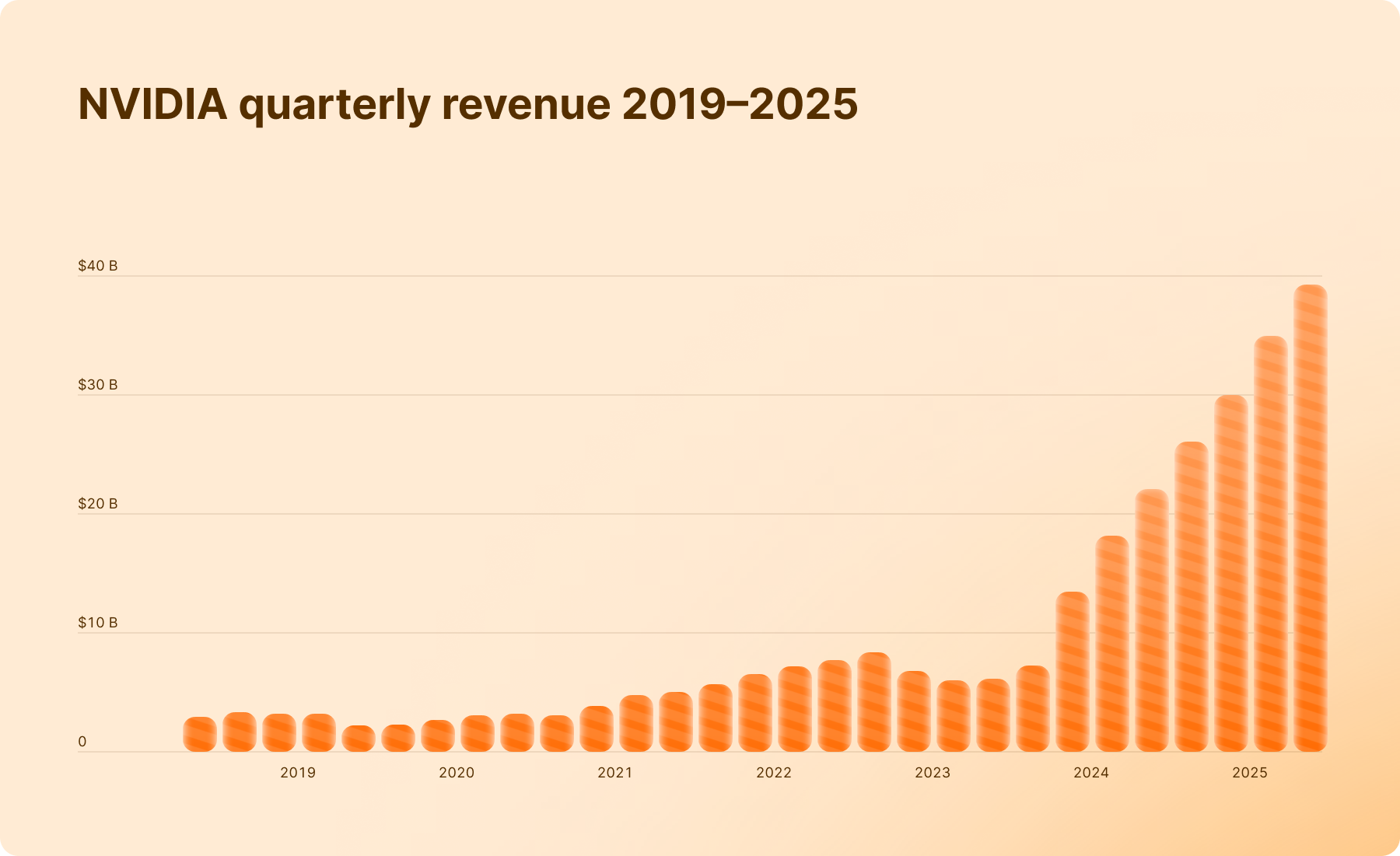

NVIDIA Corp. (NVDA) — What to Watch

It’s fair to say that Nvidia is THE most important stock in this entire story since it has become the central supplier of AI infrastructure.

- Data center and AI chip revenue

Current projections are ~70% YoY growth. The focus has shifted from “Will they buy?” to “Can Nvidia ship fast enough?”

- ≥80% YoY growth (EPS ≥1.85) → Strongly bullish: Shows very strong demand for Nvidia’s AI chips.

- 75–79% growth (EPS ~1.71) → Neutral: In line with expectations.

- <70% growth (EPS <1.60) → Bearish: May signal supply issues or more competition from companies building their own AI chips.

- Gross margins

Strong margins indicate sustained pricing power amid surging demand for AI chips.

- Above 73% → strong pricing power.

- Below 73% → possible pressure on profits.

- Next-gen chips

The focus is now on the Rubin platform — the most powerful AI supercomputer. Watch for updates on its 3nm production timeline — delays could slow the stock’s momentum.

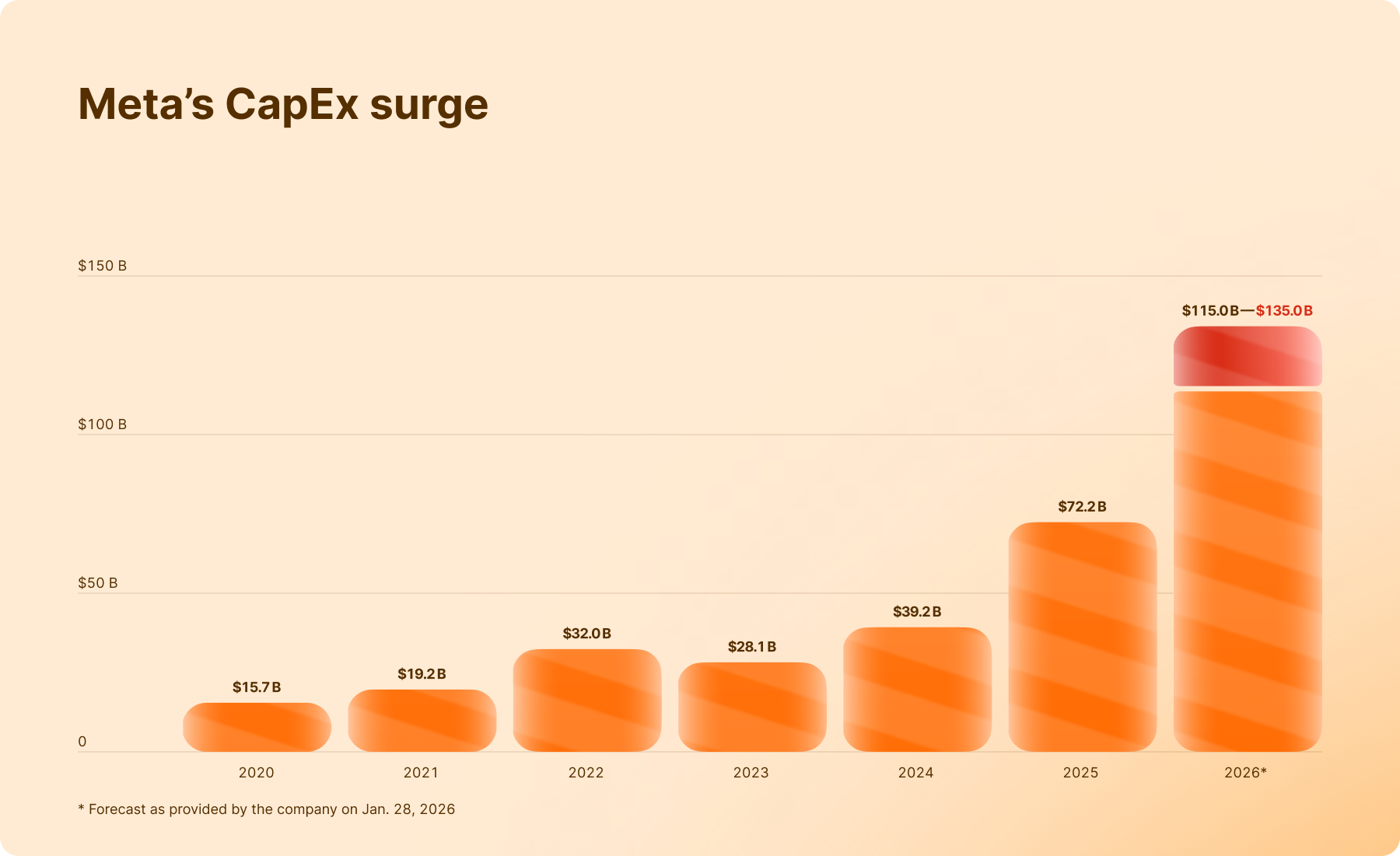

Meta Platforms Inc. (META) — What to Watch

Meta enters Q2 2026 in a much stronger position than in 2022. By shifting its focus from the metaverse to AI, the company has become a major player in the open-source AI space with its Llama 4 models.

- Advertising revenue growth

Current projections are ~28–30% YoY growth.

- ≥32% YoY growth (EPS ≥ $7.20) → Bullish: Shows strong ad revenue and successful monetization of Threads and AI tools.

- 28–31% growth (EPS ~ $6.65) → Neutral: In line with market expectations.

- <25% growth (EPS < $6.10) → Bearish: Signals slower growth and concerns about returns on Meta’s large AI investments.

- AI-driven advertising optimization

Meta is positioning Llama 4 as a major open-source AI platform, competing with models from OpenAI and Google. Watch enterprise adoption and growth from WhatsApp AI tools or model licensing.

- Positive AI adoption signals → bullish for Meta and AI stocks.

- Weak adoption or delays → could pressure the stock.

- Reality Labs / AI Glasses

Meta is shifting focus from the metaverse to AI-powered glasses (“Orion”).

- AI glasses sales: Strong growth → bullish signal.

- Reality Labs losses: Expected to peak around $19B in 2026.

- If losses increase again in 2027 guidance → bearish for the stock.

- CapEx: The $135 Billion Question

Meta is currently spending more on infrastructure than it generated in total revenue just four years ago.

- If Meta maintains 40%+ operating margins while spending $125B, it will be seen as the most efficient AI play in tech.

- If margins slip below 38%, the “spending spree” narrative will turn toxic.

Big Tech Earnings Season – Trader Guide

| Company | Expected Earnings Date | What to Watch in the Report | If Results Are Strong | If Results Are Mixed | If Results Are Weak | Other Assets That May Move |

| Alphabet (GOOGL) | ~Apr 23–25, 2026 | Google Cloud growth (~25% expected), Advertising revenue ($75B–$78B target), AI CapEx ($175B–$185B) | Cloud >40% growth and strong ad revenue → sector-wide AI rally | Cloud ~35–39% growth → steady outlook | Cloud <30% growth → concerns over AI monetization | Nvidia, AMD, S&P500 |

| Microsoft (MSFT) | ~Apr 28–30, 2026 | Azure growth (~37–38%), AI revenue contribution, Maia 200 chip rollout, forward guidance | Azure ≥40% growth → strong AI demand and enterprise cloud expansion | Growth 37–39% → stable expectations | Growth <35% → fears AI spending exceeds revenue | AI stocks, cloud sector, S&P500 |

| Tesla (TSLA) | ~Apr 21, 2026 | Vehicle deliveries, automotive margins, robotaxi/Cybercab progress, Optimus robot updates | ≥5% delivery growth and margins >18% → improving EV demand | Flat deliveries and stable margins → neutral outlook | Negative growth and margins near 15% → weak EV demand | EV stocks, battery suppliers, AI/robotics sector |

| Amazon (AMZN) | ~April 30–May 1, 2026 | AWS growth (~24% expected), retail ad revenue (> $18B bullish), AI infrastructure spending | AWS ≥28% growth → strong AI cloud demand | AWS ~24–27% growth → steady performance | AWS <22% growth → fears AI investment not paying off | Nvidia, semiconductor stocks, cloud sector |

| Apple (AAPL) | ~April 30–May 1, 2026 | iPhone 17 demand, Services growth (>14%), China sales, Siri AI adoption | ≥15% growth → strong device demand and AI cycle | ~10–14% growth → in line with expectations | <8% growth → weak demand or China slowdown | Nasdaq, smartphone supply chain |

| Nvidia (NVDA) | ~May 20, 2026 | Data center revenue (~70% growth), margins (>73%), Rubin chip platform updates | ≥80% growth → confirms AI supercycle | 75–79% growth → expectations met | <70% growth → supply issues or rising competition | AI sector, semiconductor stocks, cloud providers |

| Meta (META) | ~Apr 29–May 1, 2026 | Ad revenue growth (~28–30%), Llama AI adoption, Reality Labs spending, AI glasses | ≥32% growth and strong AI monetization → bul |

Quick Tips for Traders During Earnings Season

💡 Earnings order matters — Big Tech reports across several weeks, and each report influences expectations for the next one. For example, strong cloud spending reported by Microsoft or Amazon often signals strong demand for Nvidia chips later in the season.

💡 Trade the entire basket instead of individual stocks — find the Magnificent 7 asset in your traderoom.

💡 Strong earnings from several tech companies → AI stocks, semiconductor companies, and the Nasdaq index may rally together

💡 Weak results from large companies → Nasdaq, growth stocks, and crypto may fall

💡 Big AI spending announced → Semiconductor stocks often rise

💡 Weak consumer demand signals → Retail and consumer tech may drop

Final Thoughts

Big Tech earnings season remains one of the most influential periods in global financial markets. The results published by Alphabet, Microsoft, Apple, Nvidia, Meta, Tesla, and Amazon offer critical insights into the trajectory of technology innovation, consumer demand, and corporate investment.

For traders, these earnings reports provide more than just company updates — they offer a window into the future direction of the digital economy.