Dollar General (DG) Stock is an American discount retail chain. The company separates its operations into four distinct categories, which include highly consumable, seasonal, home products and basic clothing. As of February 2017, DG operates more than 13 320 stores all over the United States. It is expected to report its first-quarter earnings on 1 June 2017. Consensus EPS for the for the quarter is 0.99%, 4% down YoY. Earnings Whisper is $1.01.

Performance indicators

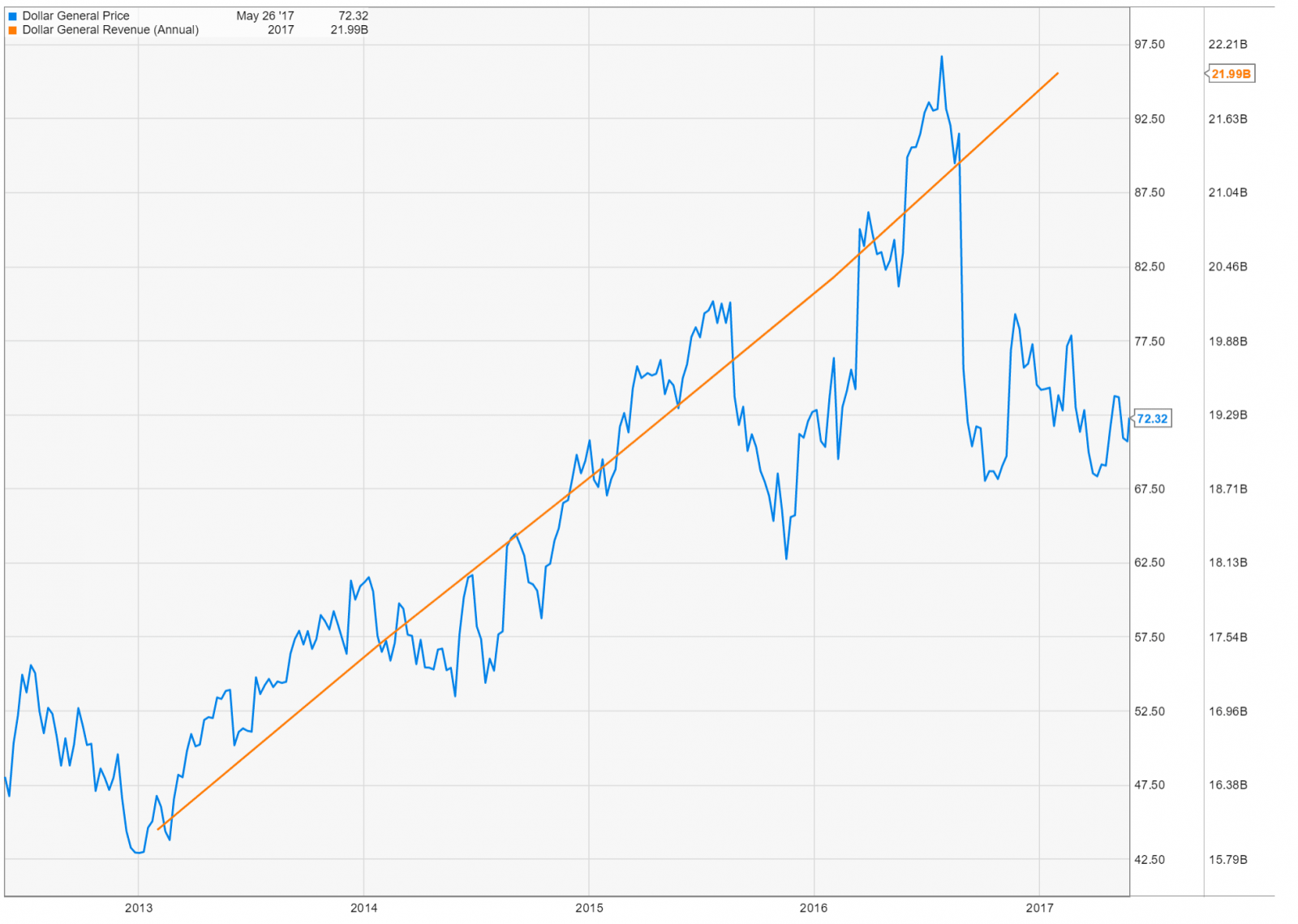

| 52 Week High-Low | $96.88 – $66.50 |

| Dividend / Div Yld | $1.04 / 1.44% |

| EV/EBITDA Annual | 9.17 |

| Consensus EPS forecast Q1/17 | $0.99 |

| Reported EPS Q1/16 | $1.03 |

| Forward PE | 16.26 |

Threats and weaknesses

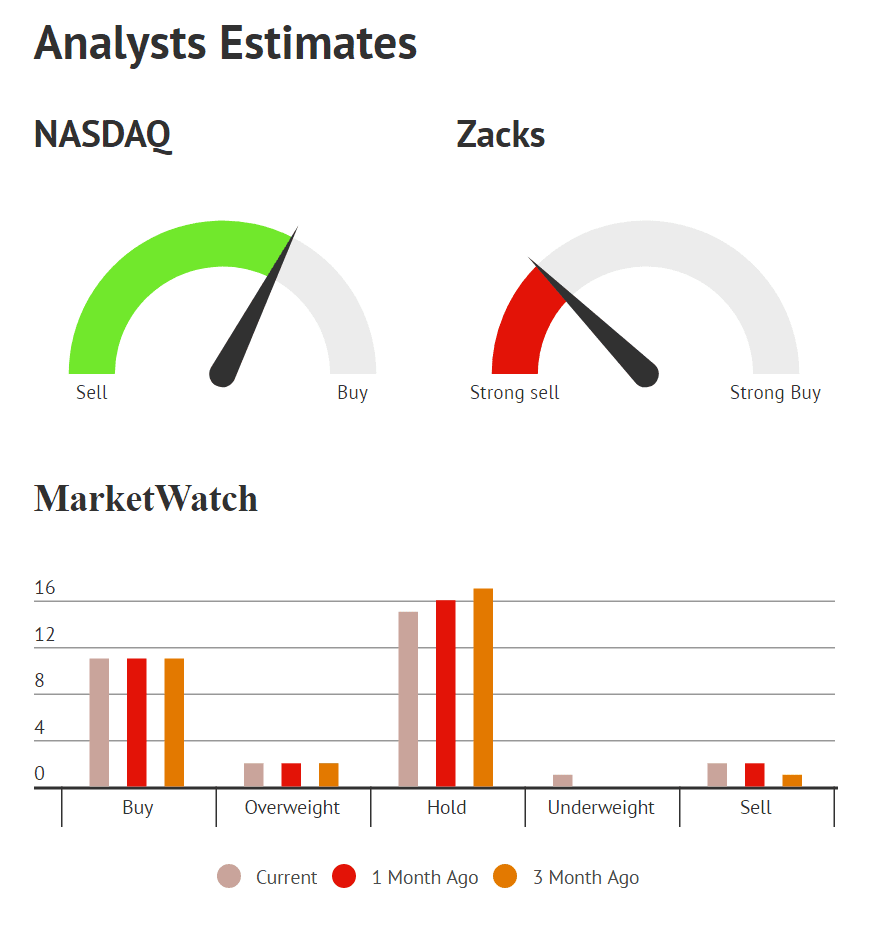

The company is rated “Sell” by Zacks which can be a good enough reason not to include it in a long-term portfolio. Other experts, however, are not so sure about DG’s “inevitable” depreciation. Still, there are enough reasons to get read of the Dollar General stocks.

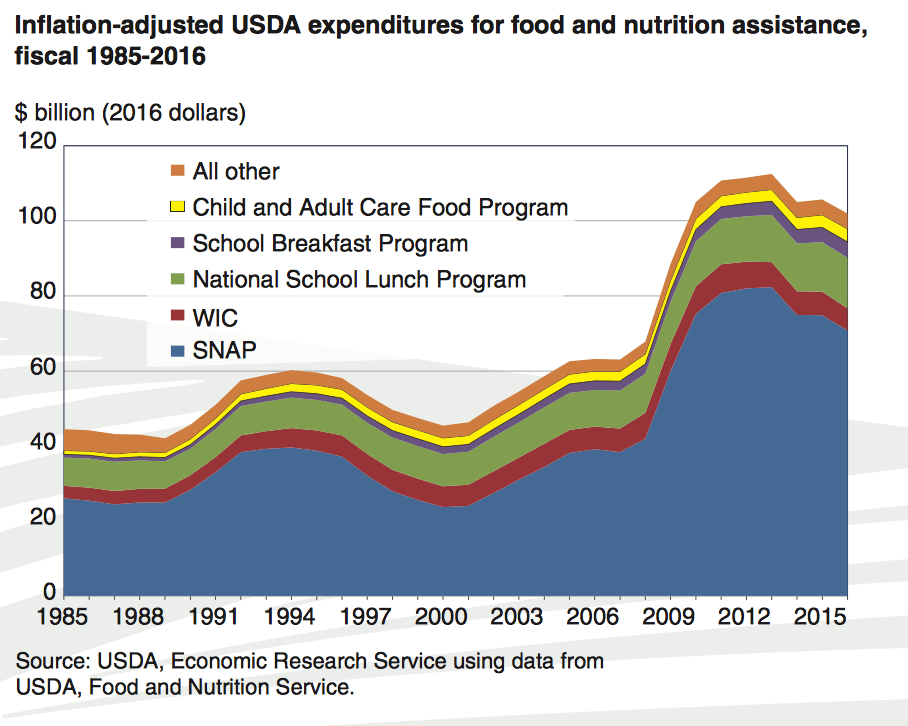

SNAP benefit cuts. Financial austerity and overall conservative economic policy, promoted by Donald Trump can lead to a significant income drop of the least prosperous segments of the population. Food stamp program is expected to lose up to $193 billion (approximately 25% of the total financing). With less government support, certain groups of consumers will inevitably spend less in retail stores. Hi-end products can be expected to be especially affected.

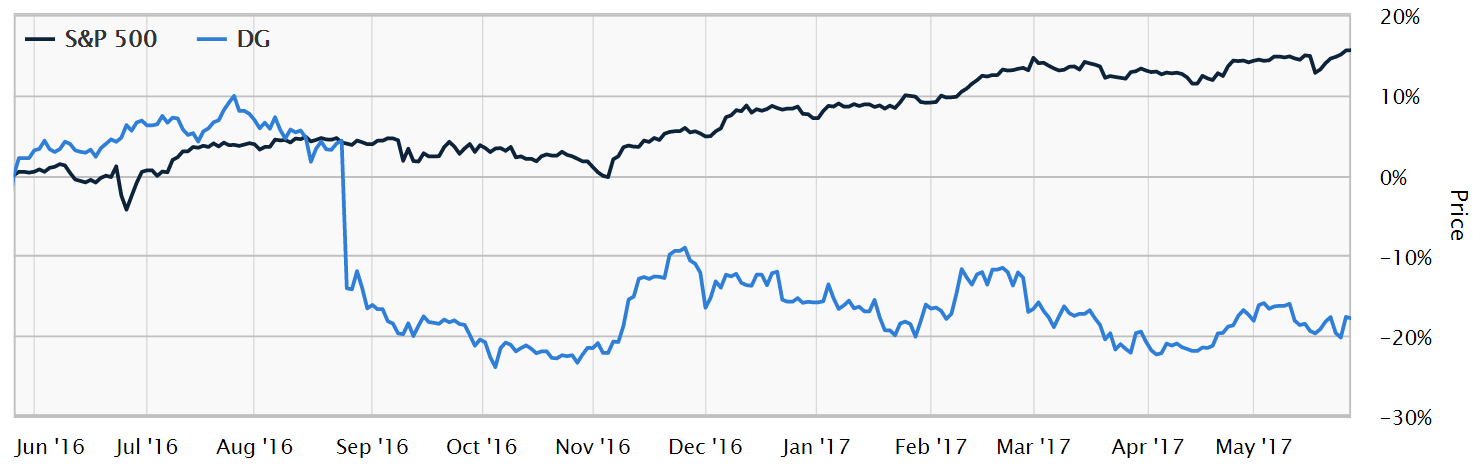

Unsatisfactory past stock performance. President-initiated economic reforms are not the only factor to consider before investing in DG stocks. In the past one year, the company has lost 20% of its market value, lagging behind the industry and the sector, in which it operates. Retail — Discount & Variety has decreased only 0.4%, while Retail — Wholesale demonstrated an impressive growth of 15%.

Macroeconomic factors. The retail industry in general and DG, in particular, are vulnerable to the impact of macroeconomic factors. Exchange and interest rates fluctuations, unemployment, availability of credit and many other metrics have a lot to do with the profitability of Dollar General’s business. Though Trump’s stock market gain in the first 100 days tops Reagan’s, it is still questionable whether the momentum is here to stay.

Tough competition. Discount retail merchandise sector is not easy to operate in. DG faces competition from Wal-Mart, Target, Dollar Tree, and Fred’s. Competition is always connected with higher marketing expenses. Online retailers pose a real threat not only to Dollar General but also to the way the retail industry operates right now.

Opportunities and strengths

Company’s dedication to long-term growth and cost-efficiency initiatives mean a lot of opportunities for increasing capitalization.

Growth initiatives. A number of cost-cutting and sales-boosting initiatives have been initiated by the company’s management, which are all destined to provide some financial results. Effective inventory management, sound pricing policy, and other performance-related initiatives constitute a competitive advantage. Annual EPS growth target is set at the 10–15% level with net sales increase at around 7 to 10%.

Sales performance. Comparable-store sales grew for 27 consecutive years. In fiscal 2017, the metric is expected to gain additional 2%. Solid growth figures that the company was able to show throughout the years and its dedication to improving the quality of the business and its profitability can speak in favor of DG stock prices growth.

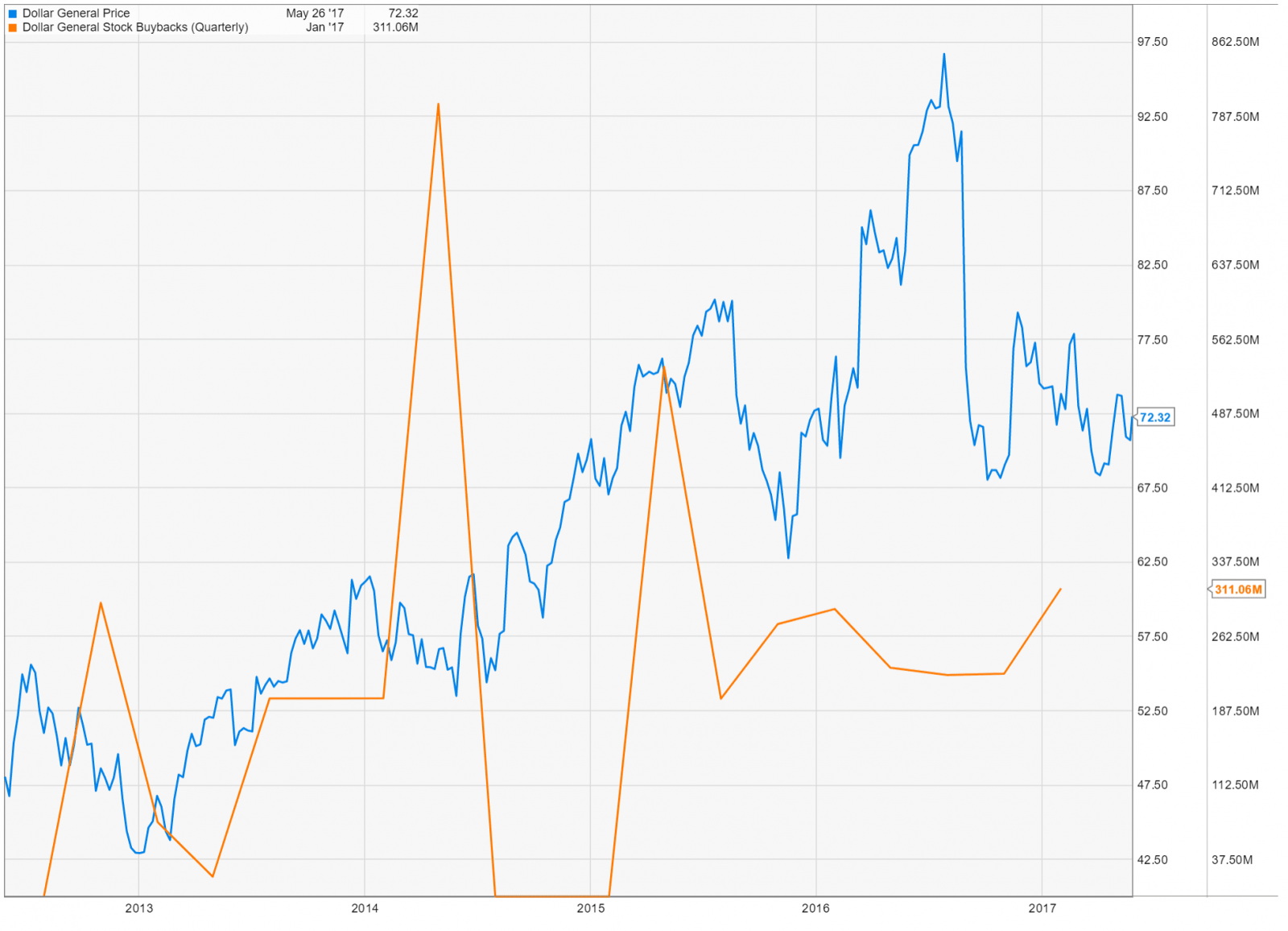

Repurchase policy. In 2016, Dollar General bought back 12.4 million shares totaling $990 million. Initiated in December 2011, the repurchase program brought back to the company over 74.4 million shares worth $4.6 billion. $450 million are expected to be spent on this initiative during fiscal 2017.

Growing number of outlets. With 900 new outlets opened and 906 remodeled in 2016, Dollar General shows an impressive growth in terms of store capacity. It can also mean that the market is currently far from being oversaturated, which leaves more room for competing retail chains.

Conclusion

DG cannot be guaranteed to deliver positive earnings surprise based on the past performance and analyst estimates. The company operates in a tough and highly competitive industry with new arising players and uncertain macroeconomic conditions. Political changes in Washington can lead to a dramatic drop in consumer products, sold to the least protected segments of the American societies. At the same time, Dollar General effectively operates its existing retail store chain and regularly adds both to the number of outlets and shareholders’ value.

The direction, in which DG stock prices will move after the earnings report is released will depend on the data, disclosed in it.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}