Last week was full of bond repricing as all government yields were back to 12th of May’s levels. “Targeting 2% inflation vs Symmetric 2% objective” was the title of my report 3 weeks ago. I was pointing to the fact that FED stopped regarding 2% inflation, as a level that would want to reach as close to, but bellow (like ECB’s communication), and started regarding it as a mean target (2% is the middle, a symmetrically above and below range is the desired level of inflation).

My interpretation has been that both central bank’s yields and the correlated government bond yields would not increase as aggressively as they did since the beginning of 2018 and that was my main reasoning to jump off from long haven trades. It took 17 days and Wednesday’s release of minutes of FED’s meeting for the markets to start pricing this new reality. On the one hand bond yields are back to 12th of May’s levels but on the other hand, haven currencies (USD, JPY) strengthened even more.

Major last week’s events:

- Korea: On Tuesday Moon (South Korea) visited Trump, on Wednesday North Korea demolished the nuclear site Punggye-ri (non-expert foreign journalists witnessed the event). On Thursday Trump announced that he is out of the North Korea-USA summit, scheduled to happen on the 12th of June at Singapore. North Korea’s reaction was prudent and on Friday Trump said that the summit is not yet dead. On Saturday North and South Korea leaders met to salvage the North Korea-USA summit.

- Tariffs front: Week began with an understanding that trade war is off. I can’t tell how crucial was the ZTE lifting of sanctions for the change of tide, yet US deputies were referring to the ZTE issue as an enforcement action, that could be resolved. On Thursday, China was dis-invited from international military exercise at the Pacific Ocean, and Trump is now targeting for a 10% cut of EU steel and aluminum imports

- Iran Deal: Following the visit to Russia, it was China’s turn to host Merkel(Germany) to talk Iran and trade

- Italy: Political situation is getting similar with the 2015 situation of Greece, when the government was communicating unrealistic economic agenda, like the contemporaneous (with Euro) issuance of certificates backed by future tax transactions.

- Cryptos: Total market cap at 337B$, another 10% decrease from last week

My Forecasts:

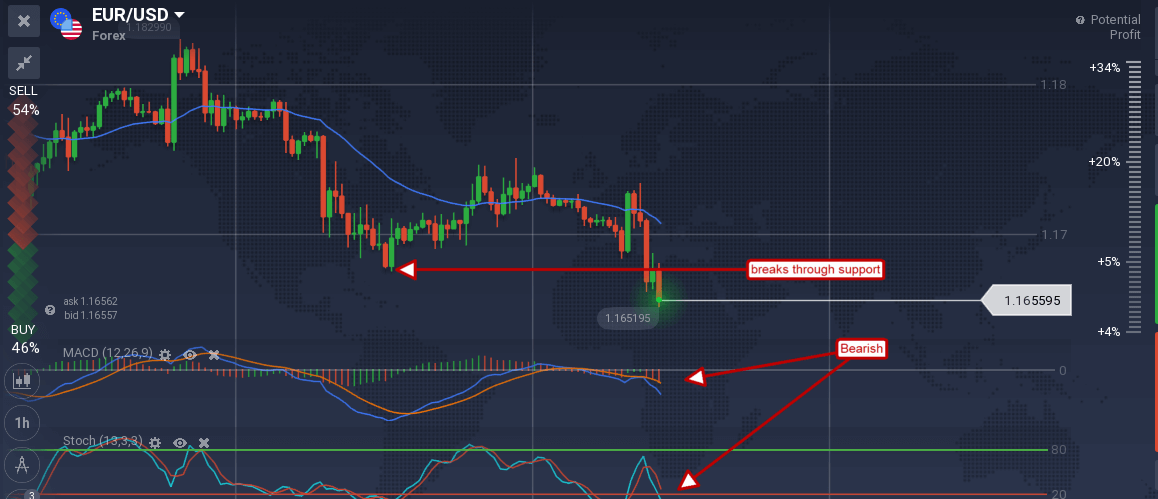

Last week’s trading ideas played bad. Nothing was offered for CAD, levels were not triggered for EUR/JPY and AUD/USD pairs, AUD/JPY was only nice for the first 14 hours and GBP/JPY was a complete blunder. The only argument that materialized was EUR/USD would stop at 1.1660~1.1600 levels, which is something that is yet to be proven, as the pair is currently at 1.1650 level.

Major next week events:

- Wednesday’s Monetary meeting of Bank of Canada.

- G7 meeting of Finance Ministers and Central Bank Governors on Thursday and Friday, one week before the scheduled G7 Leaders’ summit at Quebec Canada. Investments in developing countries is on the agenda. Remember that on the latest G20 meeting, risk-off environment was triggered

- Keep in mind the OPEC’s meeting in Vienna, scheduled on the 22nd of June

JPY

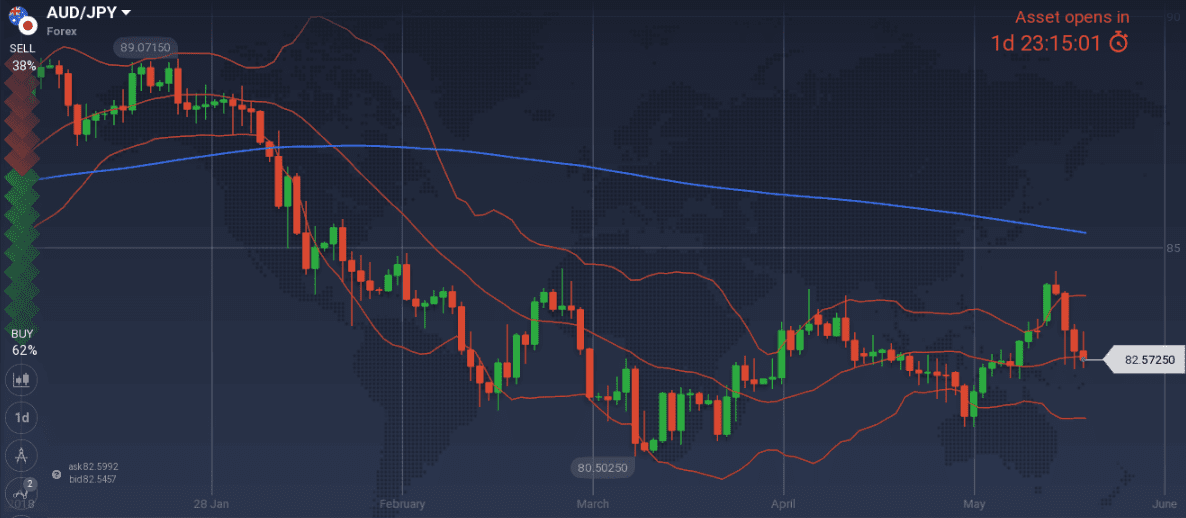

Extremely frustrated to see the safe haven JPY gaining ground across the board as I was out of these trades. The EUR/JPY 132.39 never triggered to enter, and the long 82.75~82.65 AUD/JPY trade turned red despite the fact that it looked perfect for almost 14 hours (up until 0:00GMT Wednesday morning)

Snapshot unchanged:

- Inflation (excluding food-National core CPI) at 0.7% (vs 2.0% target and BOJ’s members expectation of 1.2~1.3% within 2018), BOJ rate at -0.1%

- GDP at 0.90% annual, -0.2% q/q, 10Y Government bonds yield at 0.04% (-2bps w/w) vs BOJ’s target of 0.00% level

- Unemployment at 2.5% (lowest levels since 1993)

Strengths of JPY:

- Extended period or unpredictable events helps the haven status of JPY

- QQE set to stay in place up until 2020 or beyond.

- 5 times higher trade balance than expected, at 0.55T JPY

- one more negative week for equities is probable

Weaknesses of JPY:

- Strong technical levels need to be crossed for JPY to extend it’s strength (127.53 EUR/JPY, 108.58 USD/JPY, 82.37 AUD/JPY) At current levels I am opening no trade in favor of JPY and I note that I am already committed with long AUD/JPY

- latest negative GDP reading

Watch:

- No market moving announcements are expected

- Next Monetary Meeting on 15th of June

CAD

I offer no trading idea for CAD, as economy is growing at full potential and the only thing I want to focus on is for any indication of increased lending.

Snapshot unchanged except from bond yields:

- Inflation at 2.2% (vs 1.0%~3.0% target range), BOC rate at 1.25% (3 hikes so far). Note BOC’s confidence on neutral rate within 2.5%~3.5% range.

- GDP at 2.9% annual (near potential GDP), 0.4% qoq, 10Y Government bonds yield at 2.3549% (-14bps w/w)

- Unemployment at 5.8% and expected to decrease further.

Strengths of USD/CAD, weakness of CAD:

- Terms of trade (latest reading -4.1B CAD) favors USD

- last Friday’s south moves of oil. Remember that the correlation between CAD and oil, used to be positive and strong in the past (i.e. both moved with the same direction). However, during the last weeks the relation at insignificant levels (now at -0.35)

- Nafta talks that have not been materialized

Weaknesses of USD/CAD, strengths of CAD:

- Technically significant levels have been approached that would need more news for the USD/CAD uptrend to continue.

Watch:

- Wednesday’s 15:00GMT Monetary meeting of Bank of Canada and the release of Current Account number, 90minutes before it. No rate hike is expected, especially since inflation has moved lower by 0.1%.

- Thursday’s 13.30GMT GDP reading.

- Friday’s 14.30GMT Manufacturing PMI

AUD

I keep my previous week’s long AUD/USD bias, but could only build a position at 0.7474 or even 0.7426 levels.

Snapshot unchanged except from bond yields:

- Inflation at 1.9% (vs 2.0~3.0% target), RBA ‘s rate at 1.50% (no hike so far)

- GDP at 2.4% growth (3.0% could be achieved within 2018 and 2019 according to RBA), 10y Bond yields at 2.79% (-11 bps w/w)

- Unemployment increased slightly to 5.6% but is expected to decline.

Strengths:

- improved trade balance and increased building approvals

- improved business confidence

- China’s good performance

Weaknesses:

- household consumption is a source of uncertainty. Anything that quantifies household consumption (credit growth, wage growth, private capital expenditure) should be noted in the coming months. Latest reading of wages growth does not support AUD strengthening

- the 0.7580~0.7600 zone is behaving as a strong resistance.

Watch:

- Thursday’s 2.30GMT Private Capital Expenditure q/q

- Next Monetary Meeting on 5th of June

USD

10year Government Bond is back below 3%, markets are no more pricing aggressive rate hikes, but on the other hand USD got stronger and next FED’s monetary meeting could well include a rate hike, as macro announcements are still beating expectations.

In the past, I have noted (referring to AUD) that it’s better to say nothing when you have nothing to say. A week after that remark, I had managed to offer a view that had hit bulls-eye. For now, I will do the same with USD and offer no view. It was frustrating to not gaining from the extended last week’s USD gains, as I have closed long positions, but now even more significant technical levels need to be crossed, for the move to be extended.

Snapshot unchanged except from bond yields:

- Inflation (Core PCE) at 1.9% (vs 2.0 target and 1.9% FED’s expectations), FED ‘s rate at 1.75%. 6 hikes so far in the business cycle and another 6 hikes expected by the end of 2019, to reach 3.25%. FED’s view of long run rate remains at 2.75%~3.00%

- GDP at 2.9% growth (FED expects 2.7% in 2018), 10y Bond yields at 2.93% (-13bps w/w)

- Unemployment at 3.9% and expected to fall to 3.8% in 2018

Strengths of USD:

- strong macros (PMI Manufacturing, PMI Services, Durable Goods orders)

- geopolitical risk (possible cancellation of North Korea-USA summit, opposing stance of USA and EU on Iran deal, China trade talks)

Weaknesses of USD:

- USD/CNY, EUR/USD, USD future index need to cross significant technical levels for USD to advance more

- bond yields are showing that they have found their ceiling

- Tiny decrease of m/m home sales (-3%) and a consumer sentiment that is falling from March’s highs, when Americans were living the positive effects of the new tax law at their pockets.

Watch:

- Monday is a Bank Holiday

- Tuesday’s 15.00GMT Consumer Confidence. A lower than 128.2 reading does not help the continuation of USD strengthening.

- Wednesday’s 13.30GMT second release of GDP q/q reading and Goods Trade Balance reading. It is unlikely to see improved readings that would fuel USD further strengthening.

- Friday’s average hourly earnings m/m and unemployment that could fuel USD strengthening.

- Next Monetary Meeting on 13th of June.

EUR

The possibility of EUR/USD beginning to consolidate in current levels (1.1660~1.1600) is still valid and I could well open some small long EUR/USD trades at the opening of Tuesday’s European session at 9.00GMT with the intention to exit at 1.1750.

Snapshot unchanged:

- Annual Core CPI Inflation at 0.7% (vs 2.0% target), ECB ‘s rate at 0.00%

- GDP at 2.5% growth (OPEC expects a 2.2% reading), 10y Bond yields of EFSF at -0.44% (-1bps w/w), 10y German Bond yields at 0.41% (-16bps w/w)

- Unemployment at 8.5%

Strengths of EUR/USD:

- the pair has already approached technically significant levels and additional bad news would need to come so that the downtrend is fueled. Last week the bad news came from both PMI Manufacturing and PMI Services. This week, the continuation of bad news is unlikely and current levels are even more significant

- Despite disappointing macro announcement, the sentiment remains high

Weaknesses of EUR/USD:

- political situation in Italy.

- the different point in the cycle between US and EU economy

Watch:

- Tuesday’s 9.00GMT M3 Money supply and Private loans that could give a reason for EUR to get stronger

- Thursday’s 10:00GMT Inflation and Unemployment readings.

- Next Monetary Meeting on 14th of June

GBP

UK’s macro announcements are disappointing and the long GBPJPY trade had been a complete blunder. (My second bad call since the beginning of this periodic report). Wednesday’s decreased inflation readings could only help to decide to take losses and exit the trade.

Snapshot is worsening:

- Inflation at 2.4% (vs 2.0% target), BOE ‘s rate at 0.50% (no hike expected in 2018)

- GDP at 1.2% growth (vs 1.4% previously vs 1.5% OPEC’s estimates), 10y Bond yields at 1.32% (-18bps w/w)

- Record low unemployment at 4.2% (BOE expects to fall further in Q2)

Strengths:

- the bad weather narrative regarding UK’s economy in 1Q18 may prove to be true.

- latest retail sales m/m increase at 1.6%

Weaknesses:

- decreasing inflation readings that postpone rate hikes

- decreasing bond yields

- Monday is a Bank Holiday

- Thursday’s 9:30GMT M4 money supply. GBP bulls will only keep their hope alive with a highly unlikely positive number.

- Next Monetary Decision on 21 June.