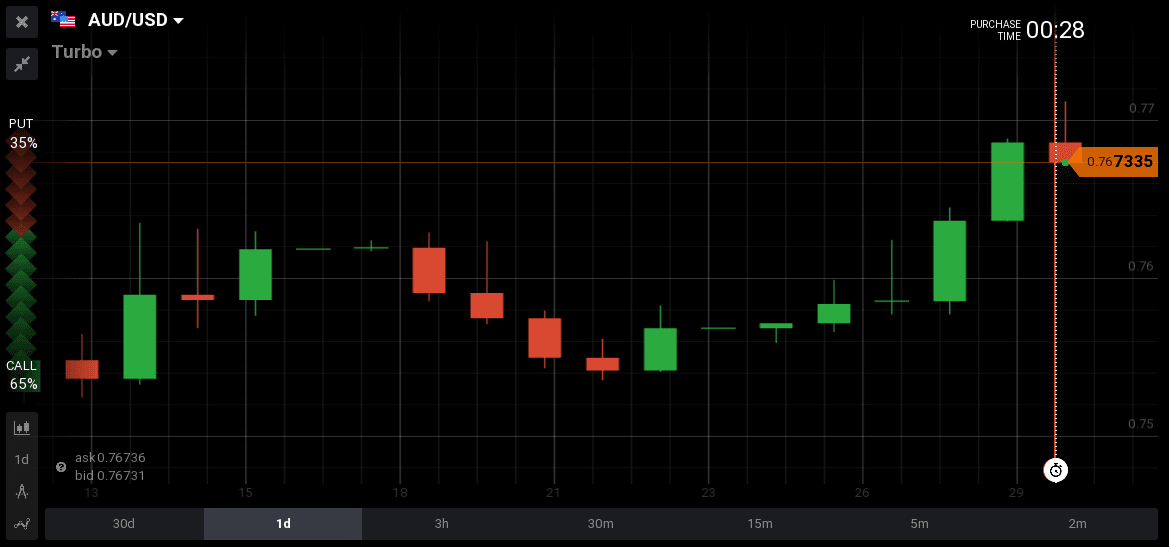

The investors and traders are keep selling US Dollars and the US Dollar Index reached a one month low with a reading of 95.27. There are numerous explanations for this, fundamental, political and behavioral finance perceptions. But our focus is on the fundamental analysis.

Australian Dollar

New Home Sales for the month of May 2017 were better than expected with a reading of 1.1% compared to the previous reading of 0.8%. This growing housing market and the fact of rising commodities prices helped the AUD/USD move 0.58% higher, from 0.7636 to 0.7689.

New Home Sales for the month of May 2017 were better than expected with a reading of 1.1% compared to the previous reading of 0.8%. This growing housing market and the fact of rising commodities prices helped the AUD/USD move 0.58% higher, from 0.7636 to 0.7689.

It is a strong trend as the appreciation of the Australian Dollar against the US Dollar continues for over a week having reached from 0.7540 to 0.7715.

Euro

The German GfK Consumer Confidence Survey reading was a bit higher than the forecast with a reading of 10.6 compared to the estimate of 10.4, and the German Consumer Price Index was also higher than the forecast, but a series of other economic data for the month of June, the Euro-Zone Economic Confidence, Euro-Zone Business Climate Indicator and Euro-Zone Services Confidence all showed an improvement in business and economic outlook for the European economy.

The German GfK Consumer Confidence Survey reading was a bit higher than the forecast with a reading of 10.6 compared to the estimate of 10.4, and the German Consumer Price Index was also higher than the forecast, but a series of other economic data for the month of June, the Euro-Zone Economic Confidence, Euro-Zone Business Climate Indicator and Euro-Zone Services Confidence all showed an improvement in business and economic outlook for the European economy.

The EUR/USD continued its rally for the 3rd consecutive day moving up 0.54% from 1.1377 to 1.1445.

British Pound

Net Consumer Credit and Mortgage Approvals both increased in May supporting the rally in the GBP/USD, up 0.64% from 1.2938 to 1.3014. The UK housing market shows strength as seen yesterday with higher housing prices, and these high inflationary pressures support the comments from Bank of England Governor Mark Carney, about the possibility of raising interest rates soon to fight inflation.

Net Consumer Credit and Mortgage Approvals both increased in May supporting the rally in the GBP/USD, up 0.64% from 1.2938 to 1.3014. The UK housing market shows strength as seen yesterday with higher housing prices, and these high inflationary pressures support the comments from Bank of England Governor Mark Carney, about the possibility of raising interest rates soon to fight inflation.

US Dollar

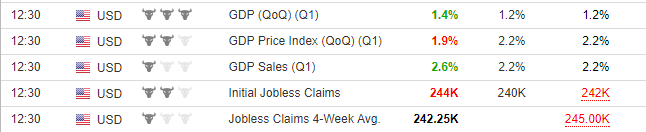

The Gross Domestic Product for the 1st quarter of the year reading was 1.4%, better than the forecast of 1.2% and Personal Consumption again for the 1st quarter was higher than the forecast. These are positive news, showing strength in consumer spending and in the general economy in terms of GDP growth.

But weekly Initial Jobless Claims and Continuing Claims were both higher than the forecasts, showing weakness for the labor market on a weekly basis. This mixed economic data was not enough to stop the selloff for the US Dollar.

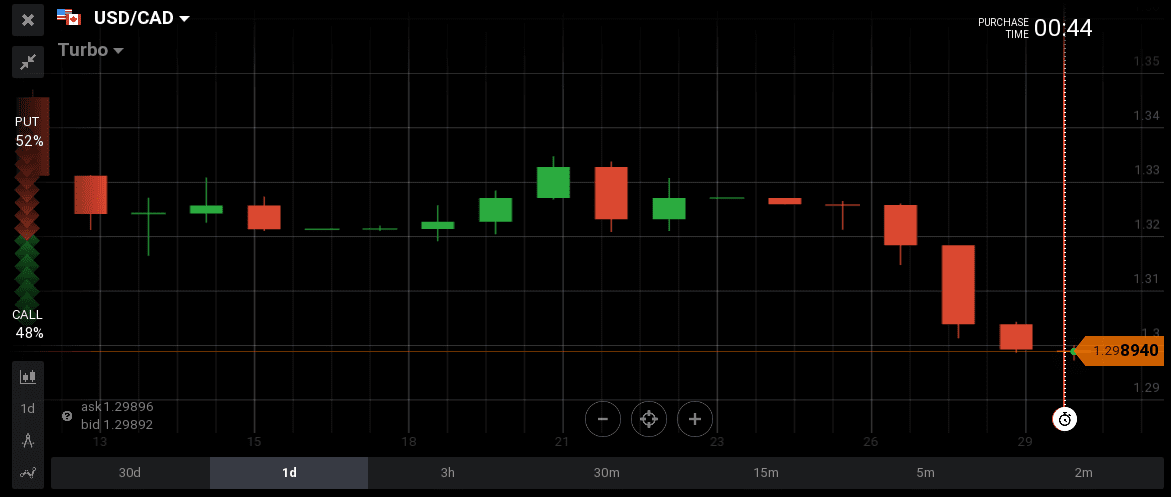

The higher oil prices supported the rally for the USD/CAD, while the gold prices fell, but not much so the USD/CHF price action can be attributed to the general US Dollar weakness.

Japanese Yen

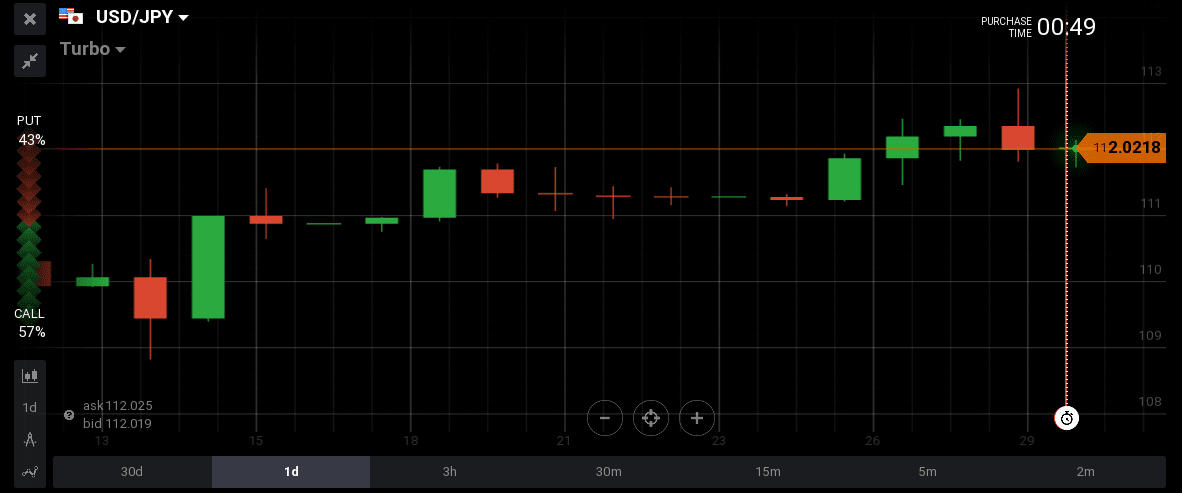

After a rally for 3 consecutive days the USD/JPY had a reversal, falling 0.27% from 112.93 to 111.82. There were a plethora of economic data about the Japanese economy with the National Consumer Price Index reading for the month of May at 0.4% less than the forecast of 0.5%, showing not any inflationary pressures for the Japanese economy.

After a rally for 3 consecutive days the USD/JPY had a reversal, falling 0.27% from 112.93 to 111.82. There were a plethora of economic data about the Japanese economy with the National Consumer Price Index reading for the month of May at 0.4% less than the forecast of 0.5%, showing not any inflationary pressures for the Japanese economy.

Even the Jobless Rate for the month of May was 3.1% higher than the forecast of 2.8%. This negative reading could indicate a contracting Japanese economy, yet with this negative economic data the Japanese Yen appreciated against the US Dollar. USD/JPY was down 0.27% from 112.93 to 111.82.

Economic calendar for Friday 30th June 2017

There are numerous important economic data today which can move the forex market. There is the German Unemployment Change and rate for the month of June, the UK Gross Domestic Product for the 1st quarter, the Euro-Zone Consumer Price Index, the Canadian Gross Domestic Product for the month of April and the US Personal Consumption Expenditure for the month of May. All these economic fundamental news can offer volatility at the last trading day of June.

{kind=link}

{kind=link}

{kind=link}